Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback

Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks  German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas

German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas  Trump and Iran Sign Framework Peace Deal in France Amid Ongoing Middle East Tensions

Trump and Iran Sign Framework Peace Deal in France Amid Ongoing Middle East Tensions  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Asian Stocks Rally as Japan and South Korea Reach Record Highs on US-Iran Peace Deal

Asian Stocks Rally as Japan and South Korea Reach Record Highs on US-Iran Peace Deal  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook

US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Oil Prices Drop as U.S.-Iran Peace Deal Eases Supply Concerns

Oil Prices Drop as U.S.-Iran Peace Deal Eases Supply Concerns  Canada Imposes 10% Tariff on Canned Vegetable Imports to Protect Domestic Industry

Canada Imposes 10% Tariff on Canned Vegetable Imports to Protect Domestic Industry

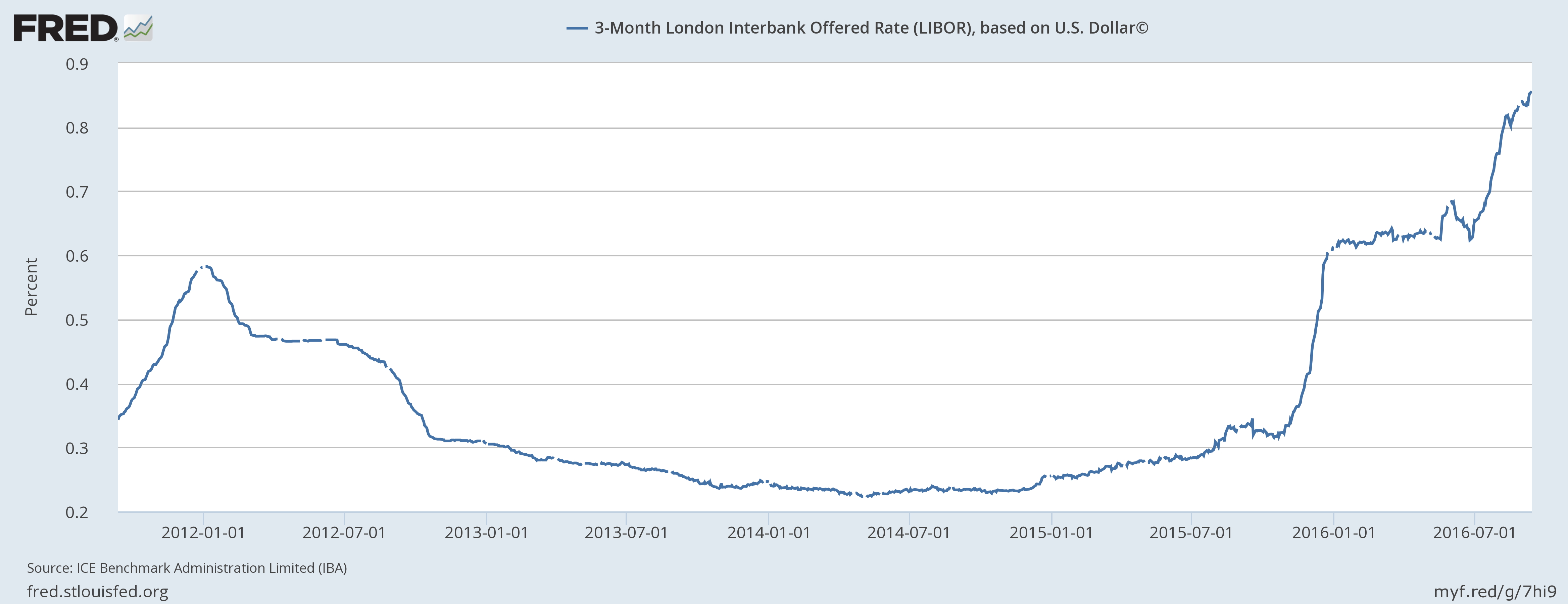

London Interbank Offered Rate (Libor) based on the U.S. dollar has already leaped to the highest level since the 2008/09 crisis and currently hovering around 0.86 percent (3-month). Compared to that, 3-month Libor based on the pound is hovering at 0.38 percent and for Euro, it is around negative 0.3 percent. So, it is clear that there are some shortages, with regard to the USD. We have listed below some of the factors that could be contributing to the rise,

- Rate hike anticipation from the U.S. Federal Reserve

- Increased risks in the financial systems that have been fuelling the demand for dollar-based funding

- The increasing number of corporate defaults, those are now much higher than 100 and at the highest since 2009.

- The major regulation changes would kick in from October on how money market funds operate and it would result in an increased cost of funding for the corporates.

Many market participants and analysts have been saying that the market is doing the tightening on behalf of the Fed, however, we feel that if the Federal Reserve increases interest rate in September (this Wednesday), even then the spread between the Libor and the U.S. treasury unlikely to shrink. We expect the Libor to move above 1 percent.