FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  BOJ Holds Rates at 1% as Inflation Outlook Eases, October Rate Hike Still Possible

BOJ Holds Rates at 1% as Inflation Outlook Eases, October Rate Hike Still Possible

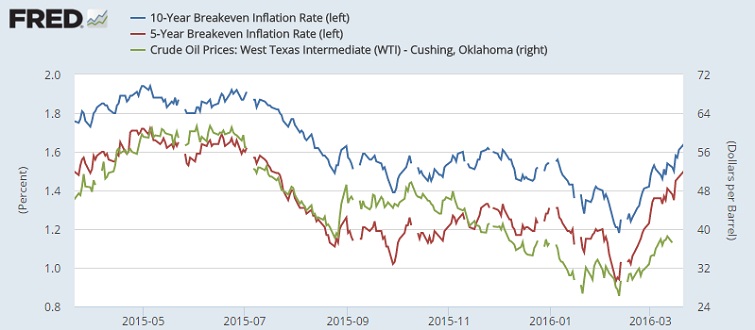

Breakeven inflation rates in United States and around the world are rising, with partial thanks to higher oil price. However, there is probably more to infer from this rising expectations rather than just to consider it as offshoot effects of recent rise in oil price.

- From recent rise in inflation expectations, which rose by 46 basis points since February it is quite evident that oil price is losing intensity of its impact over inflation expectations. That is right to be the case due to lower base effects. Going forward it is more likely that US inflation expectations will rise even if oil stabilizes at current levels. Core consumer inflation, which excludes fuel and food, already breached FED’s 2% target and hovering at 2.3%.

- As of now, 10 year break even inflation is hovering at 1.65%, while 5 year breakeven is at 1.5%. These rates are at highest since summer of 2015.

- Moreover, from the global breakeven inflation rates, we can infer that impact of oil over inflation is not similar to everywhere. In US 60 day rolling correlation between Crude and inflation expectations stand at 55%, whereas it is just 30% for Europe (taking Germany as benchmark).

So, US economy will be more prone to rate hikes, if oil rises from further, whereas Europe will need contributions from beyond oil to boost inflation.