Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

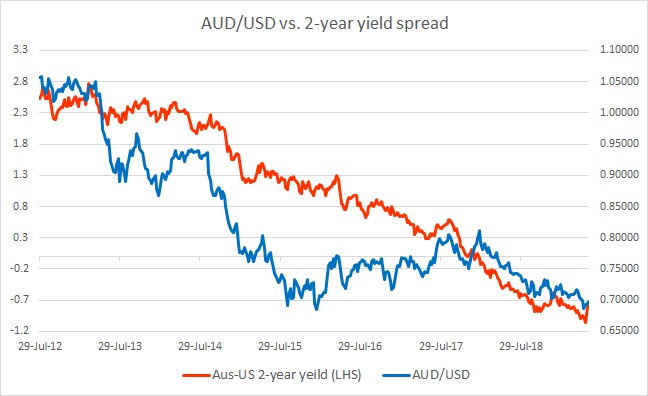

The chart above shows, how the relationship between AUD/USD and 2-year yield divergence has unfolded since 2012.

The chart above makes a clear case of closeness between the rate spread and the exchange rate. The spread between the 2-year U.S. Treasuries and the 2-year Australian government bond declined from +253 bps to -72 bps. AUD/USD responded by declining from 1.056 area to 0.729 area.

In November, we noted that the spread has reversed course and the declining Australian dollar is reducing the divergence fast and if the spread continues its reversal, at one point Aussie is likely to find support in it. The divergence got further reduced in December.

However, the reversal didn’t last long, as the Reserve Bank of Australia (RBA) added dovish comments. Since the comments, the spread has again changed course and widened from just 58 bps in December to -75 bps as of February.

While the Australian dollar ticked higher the spread further widened from -75 bps in February to -84 bps in April, in favor of the USD.

In May, the Reserve Bank of Australia (RBA) reduced rates by 25 bps, which has accelerated the yield decline in Australian 2-year government bond in anticipation of more cuts. The U.S. yields have moved lower too in anticipation of rate cuts by the U.S. Federal Reserve, which in turn narrowed the spread.

In May, the spread has narrowed to -79 bps, and Aussie s consolidating around 0.697 area.