China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

A possible bottoming out in inflation and the Fed repricing of a December hike are outright bearish and gold should rebase lower. To this end, the median Fed participant continues to look for one more hike this year, and three more to go in 2018. The 2019 median path was trimmed from three hikes to two, offsetting the somewhat hawkish near-term message.

The market expectations, however, are quite different. Still awaiting a stronger confirmation of a sustained upward trend in inflation, the market is only pricing in less than two full hikes by December 2018, which seems overly pessimistic given the upbeat economic backdrop. This complacency on the Fed is mostly due to the fact that the Fed had signaled its rate decisions would be primarily driven by inflation, which until August surprised to the downside over five consecutive months.

The repricing is already taking hold. Three weeks ago, the rate markets priced no hikes through 2018; today it’s almost two. December hike probabilities have now risen to almost 63% from 28% just two weeks ago. But we expect more.

The four Fed-related corrections so far this year averaged sell-offs of $28/oz, $58/oz, $76/oz and $84/oz each, with the current sell-off surpassing $50/oz so far. Considering the higher starting point, we believe the downside trade has room to play out further. While further weakness in the broad dollar and re-escalation of political tensions could lend some support to bullion prices, we continue to caution against holding gold as a political hedge during the global rate normalization cycle.

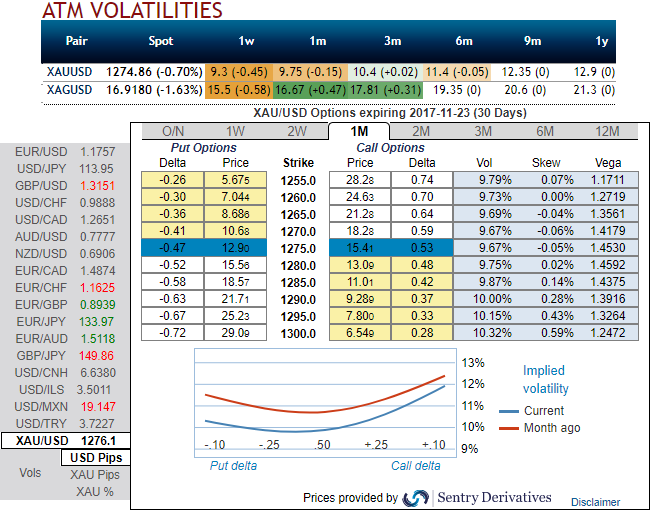

As you can observe that today’s gold price rallies have been snapped by cautious bears in as soon as the price touches $1283.64 where it sees stiff resistance at 7DMA mark.

Went short Dec’17 CME gold at a price of $1,318/oz on September 20, 2017. We continue to uphold the position for the commensurate trade target upto $1,190/oz with a strict stop 1 at $1,294/oz and stop 2 at $1,306.

Option Trade Recommendations (Credit Put Spreads):

The XAU (gold) volatility market normalized sharply (you could observe that in XAUDUSD IVs across all tenors) and IV skewness is quite favorable for ITM put option holders, synthesizing this with ongoing trend of this pair, we eye on writing overpriced in the money put options that likely to reduce hedging costs of long legs.

Hence, we foresee opportunities in writing ITM put during shrinking IVs with positive skewness to OTM calls.

At spot reference: $1275, one can also deploy diagonal credit put spreads by writing 1m (1%) in the money put while initiating longs in 3m at the money put, the structure could be constructed at the net credit.