BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

The UK labour market figures for the 3 months to July continue to paint a benign picture broadly maintaining previous pre-referendum trends. The unemployment rate held at 4.9%, as expected, a low level at which capacity constraints might typically be expected to put upward pressure on wages.

The UK central bank (BoE) responded to the recent Brexit shocks by easing in its monetary policy, to keep bank rates at record lows of 0.25%, while launching a package of measures designed to provide additional monetary stimulus that includes, among others, the purchase of up to £10 billion of UK corporate bonds and an expansion of the asset purchase program for UK government bonds of £60 billion. In today’s BOE guidance is likely to add pressure on GBP although any change in monetary policy seems unlikely.

SNB confirmed interventions during referendum night, seeing FX reserves rising in June.

Swiss interest rates remain lower than pre-Brexit levels, and the entire gov’t curve is yielding negative rates, except the 50y. Money market rates indicate 40% probability of a 25bps cut at the next meeting 15 Sep although the Swiss central bank is likely to maintain rates status quo.

Forecast: 1.2780, and in between range 1.1.2780 - 1.2505 in next 1 to 3 months respectively.

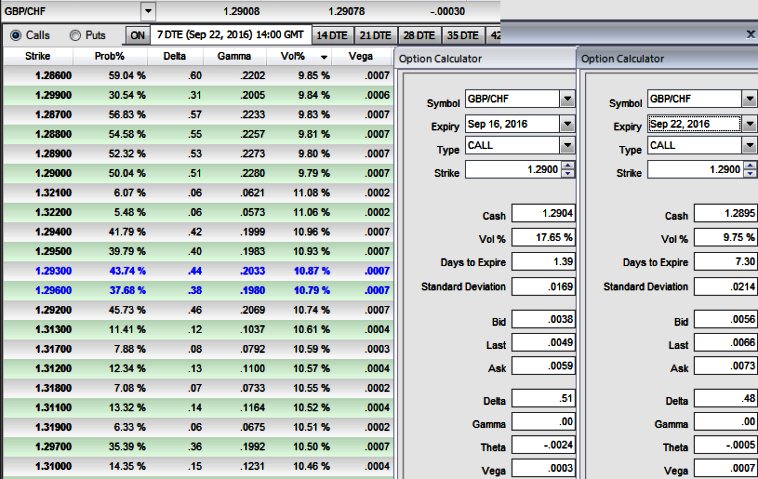

Option Trade Recommendation: Debit Call Spreads

We expect a weaker result than consensus and therefore see scope for further Sterling weakness against Swiss franc.

Execution: Go long in 2w (1%) ITM +0.67 delta call, and simultaneously short 2W (1.5%) OTM call with preferably positive theta or closer zero.

Margin: Yes, needed on short side

Rationale: The current ATM IVs are spiking at 17.21% ahead of above mentioned central bank events.

The Delta is continuously varying as the underlying spot FX fluctuates. Long options with further in-the-money (ITM) would have a higher Delta. This indicates that ITM options are worth more per pip movement in the underlying market and out-the-money options are worth less per pip.

Strategy run-through:

One can use this strategy upon the expectation of trading or even on hedging grounds that the underlying spot FX GBPCHF would rise in the long run but certainly not with drastic pace in short run. Even if it goes against, the maximum loss is limited by OTM strike price. having shorts in this strategy capitalize on reducing vols and initial premiums that we receive would finance for the long position.

Risk/Reward Profile: The profit is limited by OTM strike price, No matter how far the market moves above, the profit remains the same.