UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

The NZD has under-performed considerably post-RBNZ monetary policy and the Trumps victory. Concerns about exports, plus a stronger US dollar, are at play.

The FxWirePro NZ dollar strength index flashing up with negative 72.962 even after last weeks’ central banks easing at record 1.75%.

While NZ fundamentals remain strong, the NZD will bear a risk premium linked to the threat to Asian trade volumes from the Trump win.

There is also a minor headwind (so far) from today’s earthquakes, the extent of damage likely to take some time.

NZ events this week are second tier, apart from perhaps the GDT dairy auction on Tue. which is predicted by futures to result in a 5% rise in whole milk powder (WMP). Otherwise, there’s REINZ housing data, services PMI (Mon), Q3 retail sales volume (Tue), Q3 PPI (Thu) and ANZ consumer confidence (Thu).

On the US calendar, Oct retail sales and CPI and the first of the Nov PMIs Philly and Empire) are the main releases of note but we suspect 10 Fed speak engagements along with any fresh details on Trump’s policy agenda will be the main focus this week.

3 months: We target 0.70- based on an assumption the Fed will hike in Dec. However the persistent backdrop of global demand for high-yielding currencies is strong - if the Fed doesn’t hike, then 0.75+ is likely instead.

As more dollar rallies into X’mas FOMC are foreseen, we also target 0.6950 or lower as long as the Fed tightens to 0.625% in December.

The strategy:

We target below 0.70, based on an assumption the Fed will hike in Dec and the RBNZ’s cut is still having the room to price in. However the persistent backdrop of global demand for high-yielding currencies is strong - if the Fed either doesn’t hike or signals very gradual tightening, then 0.75+ is likely instead.

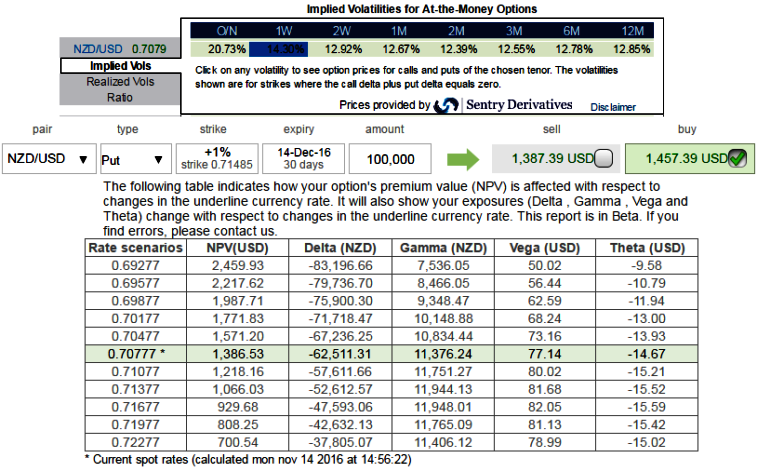

Contemplating all these underlying factors, to arrest these downside risks we advocate initiating longs in 1m (1%) ITM put option with net delta -0.71.

A higher (absolute) Delta value is desirable for an option buyer, whilst a Delta close to zero is desirable for the option seller as a buyer wants their option to become more valuable whilst a seller wants the option to become less valuable.

Rationale: Further dollar rally into December FOMC.

The FX market is still underpricing the likelihood of a Fed hike by year-end and RBNZ’s recent rate cut. We expect further gradual dollar gains into the December FOMC meeting.

Risk/return profile: No Fed cut and continued pro-carry macro environment, the key risks to the trade are that the RBNZ does not cut rates in November, the Fed does not hike by December, and the pro-carry global macro environment persists. The divergent policy expectations on the RBNZ and Fed are crucial for the trade to work.