S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online

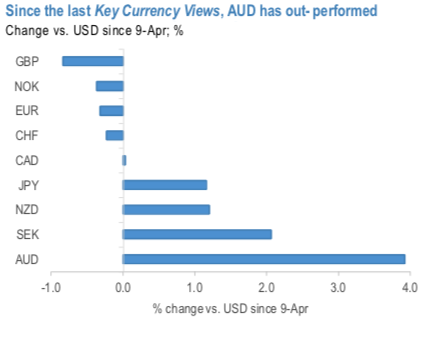

AUD has been the standout performer within G10 (refer 1st chart). Most of this rally occurred during April, and since then AUD has traded a very tight range (0.6370-0.6530). One new development for AUD has been an escalation of trade tensions with China. However, we have not made any changes to our forecasts; we see AUDUSD at 0.63 by mid-year (expecting some near term seasonal under-performance) and 0.65 by year end.

RBA is scheduled for their monetary policy for this week, of late, Aussie central bank’s policy settings have remained unchanged since being announced on 19 March. The Bank remains committed to leave the cash rate at current levels until “...progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band.” What has changed has been an easing of restrictions as Australia has made significant gains in managing the COVID-19 outbreak (refer 2nd chart). This gives us greater confidence in our central case forecast for a return to growth in 3Q’20.

The latest development for AUD has been an escalation of trade tensions with China (refer 3rd chart). Senior Chinese diplomats have recently expressed displeasure with Australia's support for an international inquiry on the origins of COVID-19 and have threatened the possibility of economic retaliation. In addition, China has raised the potential for 80% tariffs on Australian barley (in response to alleged dumping behaviour) and has this week banned imports from four Australian beef processors. The Australian government has so far played a straight bat to much of this noise, but it does serve to highlight that risks to Australia's exports to China are very asymmetric in a post COVID world where relations deteriorate and China uses economic coercion to punish Australia. This is a potentially large source of downside risk for AUD, and one that may cap any upside for AUS that exists on the basis of a relatively earlier return to economic activity, still solid iron ore prices and the RBA's "QE-lite" compared to other central banks.

We advocated shorting AUDUSD futures contracts of mid-month tenors on hedging grounds, we wish to uphold the same strategy as the underlying spot FX likely to target southwards below 0.65 levels in the medium run (spot reference: 0.6750 levels). Writers in a futures contract are expected to maintain margins in order to open and maintain a short futures position. Courtesy: JPM