Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online

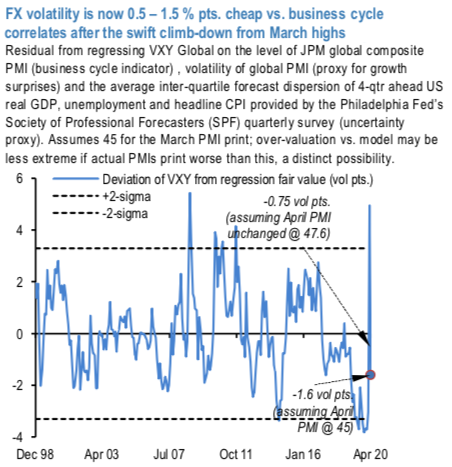

FX volatility, especially in G10, has spent most of April retracing from the manic highs of March as a plethora of Fed liquidity programs helped calm nerves in risk markets. But because the softening in vol has occurred alongside shockingly bad activity prints (European PMIs in the last week) and continued downgrade in global growth forecasts, there are now signs that this bearish reversal may have run too far: benchmarked against the level and variance of global manufacturing PMIs and macro forecast dispersion, VXY Global (9.6) screens 0.5 - 1.5 % pts too cheap depending on the projection of April Global PMI – for choice, probably the deeper of the two undershoots based on this week's G3 flash releases (refer 1st chart). It is not unreasonable to surmise that the Fed liquidity backstop may have trimmed the most disruptive of FX tails and hence the multi-sigma cyclical risk premium at the unhinged extremes of the GFC crash is perhaps not warranted this time around, but it is difficult to justify a risk discount in any asset class volatility in this growth climate (perhaps absent direct Fed purchases, but FX does not fit that description).

In addition to upside pressures on vol from the ongoing devastation in global growth, three factors are worth flagging as sources of potential spike risk -- the fallout of increased oil/commodity volatility, the rising political temperature in Europe, and the potential revival of US/China tensions. Higher commodity volatility is more impactful for commodity exporting EMs rather than G7 vols – a distinction exacerbated in the current instance by the ability of commodity exposed G10s like Australia and New Zealand to embark of QE on a scale that EMs will be hard-pressed to mimic - we are nevertheless still surprised by pockets of G7 resilience such as CAD that we would have expected ex-ante to react more forcefully to negative prompt WTI prices, and which we think are due a catch-up in coming weeks – perhaps if/when the kerfuffle around the May expiry WTI futures contract repeats next month; we buy USDCAD forward volatility this week through one-touch CAD put calendar spreads. Political risks around Europe and China both bear close watching from here.

On the former, owning EUR vol and/or risk-reversals has typically been a sub-optimal hedge against jitters in the European periphery in the past, so we are on the lookout for better value, higher-beta vol expressions over and above directional exposure already in the macro trades portfolio.

We do, however, buy some CNH forward vol this week to hedge against any abrupt deterioration in US/China relations that turns CNY-stability on its head. Given unchallenging vol levels today, no one should be surprised if some combination of these economic and political tails delivers the risk-unfriendly outcomes May is notorious for. Courtesy: JPM