Oil Prices Steady as U.S.-Iran Truce Uncertainty and Middle East Tensions Keep Markets on Edge

Oil Prices Steady as U.S.-Iran Truce Uncertainty and Middle East Tensions Keep Markets on Edge  Gold Prices Slide as Hawkish Fed and Strong Dollar Weigh on Bullion

Gold Prices Slide as Hawkish Fed and Strong Dollar Weigh on Bullion  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare

Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare  Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback

Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback  100+ Global Companies Push Governments to Prioritize Electrification for Economic Growth

100+ Global Companies Push Governments to Prioritize Electrification for Economic Growth  Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal

Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal  Dollar Holds Firm as U.S.-Iran Talks Ease Tensions, GBP/USD Slips Amid UK Political Uncertainty

Dollar Holds Firm as U.S.-Iran Talks Ease Tensions, GBP/USD Slips Amid UK Political Uncertainty  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  Asian Stocks Rally as Japan and South Korea Reach Record Highs on US-Iran Peace Deal

Asian Stocks Rally as Japan and South Korea Reach Record Highs on US-Iran Peace Deal  Gold Price Rises as Investors Weigh U.S.-Iran Talks and Fed Policy Outlook

Gold Price Rises as Investors Weigh U.S.-Iran Talks and Fed Policy Outlook  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Oil Prices Drop as U.S.-Iran Talks Ease Supply Concerns

Oil Prices Drop as U.S.-Iran Talks Ease Supply Concerns  US Stock Futures Recover as Iran Signals Progress in Peace Talks

US Stock Futures Recover as Iran Signals Progress in Peace Talks

The RBNZ said it has ended its easing cycle and will remain on hold until 2020. That will anchor the short end, although markets will not abandon their expectations for earlier tightening which means occasional spikes in the 2yr will be likely.

The long end will continue to follow mainly US yields, which we expect to rise. That means the curve steepening trend should continue.

Granted, the NZ economy is strong and dairy prices have risen, but these forces are subservient to the US dollar’s trend. Better data, but falling real rates and tightening credit keep us bearish.

We expect NZD to fall through this year, reaching 0.62 at year-end. The support to growth from migration will fade, while the RBNZ -at the very least–are likely to hold rates steady as inflation normalizes, pushing real rates materially lower.

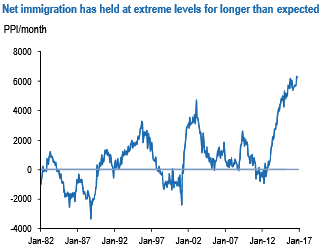

Since our NZD outlook piece in November 2016, the economy has continued to perform strongly in real terms. GDP growth was over 1% QoQ in Q3, which would see the economy rounding out the year with annual growth comfortably above 3%. Still, much of the upside surprise in activity indicators is owed to the positive supply shock from migration (see above chart).

We expect that growth impulse to fade through 2017, which would deliver growth performance more in keeping with subdued inflation, and would also remove some of the pressure on housing.

It is even easier for the RBNZ to maintain a low for long bias in an environment where spreads are widening, and delivered mortgage rates are rising. We believe the overvalued exchange rate is preventing sufficient capital inflow to the non-bank economy to compensate for a swelling current account deficit. This has resulted in leakage of NZD liquidity, and rising funding costs for the bank.

The economy is also now subject to credit tightening through numerous channels: macro-prudential constraints, widening mortgage rate spreads, and banks’ discretionary tightening of credit criteria to businesses. We now expect the RBNZ to be on hold this year, but there is a clear downside risk to the OCR in the near term.