Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Russia Stocks End Flat as MOEX Index Hits New 52-Week Low; Gold Falls and Oil Mixed

Russia Stocks End Flat as MOEX Index Hits New 52-Week Low; Gold Falls and Oil Mixed  Russian Stocks End Flat as MOEX Index Hits New 52-Week Low

Russian Stocks End Flat as MOEX Index Hits New 52-Week Low  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets

Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets  Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare

Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  US Stock Futures Recover as Iran Signals Progress in Peace Talks

US Stock Futures Recover as Iran Signals Progress in Peace Talks  France Faces Long Road to Economic Rebalancing as Weak Demand and High Rates Weigh, Says Citi

France Faces Long Road to Economic Rebalancing as Weak Demand and High Rates Weigh, Says Citi  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Trump Says No Hormuz Strait Tolls During 60-Day Iran Ceasefire

Trump Says No Hormuz Strait Tolls During 60-Day Iran Ceasefire  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

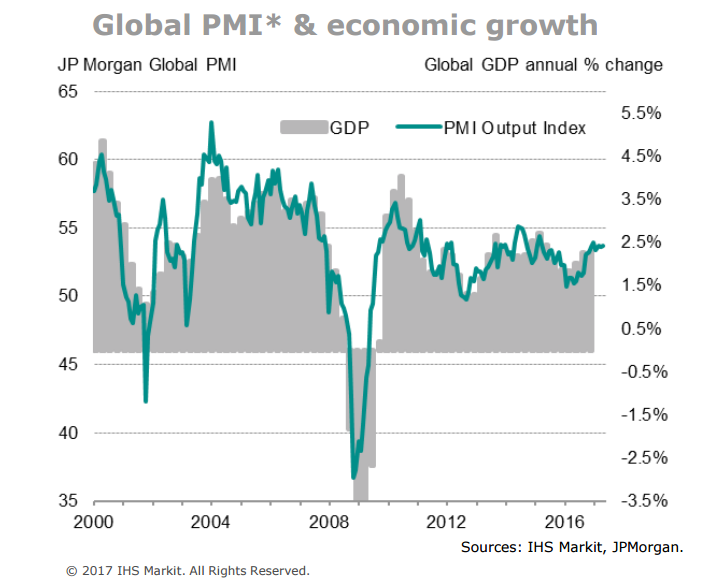

According to PMI survey data compiled by IHS Markit, JPMorgan Global PMI edged higher to 53.7 in May from 53.6 in the previous month. Both the emerging markets and the developed world signalled robust rates of economic growth. While the Emerging Market PMI rose to 52.2 in May, the second highest in 32 months, the Developed World PMI held steady at 54.3.

Growth in the developed world economies was led by Europe, followed by the UK. Relatively robust expansions were meanwhile seen in the US and Japan with both reporting faster rates of growth than April. The biggest disappointment was the on-going meagre growth rate signalled by the Caixin PMI surveys for China, where manufacturing even slid back into decline.

Data suggested that the global economy is on track for a robust second quarter, with the latest reading being broadly consistent with global GDP growing at an annual rate of 2.5 percent. That said, global PMI surveys highlighted the challenges of low cost pressures as shown by the smallest rise in worldwide factory input prices since last September. Data suggested that lower cost pressures could also feed through to consumer prices as retailers see pressure come off wholesale prices.

As political uncertainties rise across Europe, risk for sustainable growth rises. The broader mood in the market appears cautiously positive. A 25bps cut by the Fed is more or less fully priced in at this point, but the future path still represents a potential risk for the USD as investors are clearly skeptical that policy makers can deliver further tightening as focus turns to the balance sheet reduction process and weak inflationary pressures persist. And with an inconclusive election result in the UK, focus turns to Brexit negotiations which have the potential to dent prospects for UK economy.

Forex markets remained volatile on the day. GBP slumped in wake of UK election result. USD was trading firmer, up 0.7 percent on the week, extending gains for a third day. EUR broke below 1.12 against the USD as the European Central Bank (ECB) shows little risk of immediate policy change. JPY was under steady pressure with focus on the Bank of Japan (BoJ) policy meet next week.

FxWirePro's Hourly Currency Strength Index at 1200 GMT was as follows: USD Spot Index: 76.7096 (Nuetral), JPY Spot Index: -30.7466 (Nuetral), GBP Spot Index: -118.237 (Bearish), EUR Spot Index: -25.7756 (Nuetral). For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex.