Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Australia Bans Card Payment Surcharges Starting October 2025

Australia Bans Card Payment Surcharges Starting October 2025  Bank of Korea Nominee Shin Hyun-song Calls for Flexible Monetary Policy Amid Iran War Risks

Bank of Korea Nominee Shin Hyun-song Calls for Flexible Monetary Policy Amid Iran War Risks  Bank of Japan Eyes Further Rate Hikes Amid Middle East Tensions and Inflation Pressures

Bank of Japan Eyes Further Rate Hikes Amid Middle East Tensions and Inflation Pressures  Citigroup Delays Fed Rate Cut Forecast Amid Strong Jobs Data and Inflation Concerns

Citigroup Delays Fed Rate Cut Forecast Amid Strong Jobs Data and Inflation Concerns  ECB Warns of Rising Inflation Risks Amid Iran War Energy Shock

ECB Warns of Rising Inflation Risks Amid Iran War Energy Shock  India's Central Bank Holds Rates Amid Iran War Energy Shock

India's Central Bank Holds Rates Amid Iran War Energy Shock  Bank of America Maintains Forecast for Two Fed Rate Cuts in 2026 Despite Inflation Risks

Bank of America Maintains Forecast for Two Fed Rate Cuts in 2026 Despite Inflation Risks  RBI Clamps Down on Rupee NDF Activity, Banks Face Steeper Losses

RBI Clamps Down on Rupee NDF Activity, Banks Face Steeper Losses  Morgan Stanley: Fed Rate Cuts Still on Track Despite Oil-Driven Inflation

Morgan Stanley: Fed Rate Cuts Still on Track Despite Oil-Driven Inflation

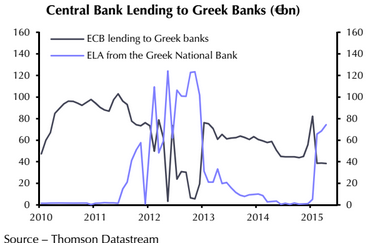

The ECB's exposure to Greece is not huge and ultimately lies with the euro-zone governments that would have to recapitalise it. But a Greek default to the ECB would be a serious blow to the Bank's credibility that could limit its ability to control inflation or support stressed bond markets in future.

The ECB is exposed to a Greek default through two direct channels. Its holdings of Greek government bonds purchased during the Securities Markets Programme (SMP) have a book value of €18bn, or 0.2% of euro-zone GDP. Chart shows that €6.7bn worth matures this summer. And its lending to Greek banks through refinancing operations was €38.5bn (0.4% of GDP) in April. So in the event of a sovereign default and associated collapse of the banking sector, the ECB could suffer losses of up to €56.5bn, wiping out its subscribed capital of €10.8bn, but not its total capital and reserves of €96bn, notes Capital Economics.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

How vulnerable is the ECB to a Greek default?

Thursday, May 28, 2015 9:01 AM UTC

Editor's Picks

- Market Data

Most Popular