BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  South Korea Central Bank Holds Interest Rates Steady Amid Inflation Concerns

South Korea Central Bank Holds Interest Rates Steady Amid Inflation Concerns  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  Gold Tumbles Below $4,400 on NFP Shock: Fed Easing Bets Crater, Sell on Rallies to $4,300

Gold Tumbles Below $4,400 on NFP Shock: Fed Easing Bets Crater, Sell on Rallies to $4,300  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

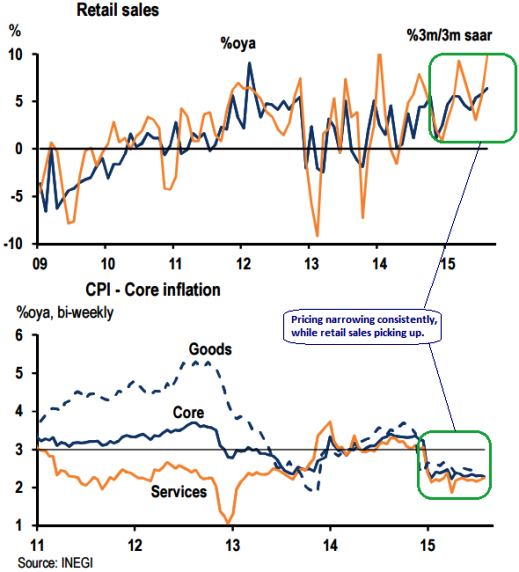

We look ahead for Banxico to focus on the benevolent macroeconomic environment (such as inflation outlook, job market, retail sales etc) in next week's policy statement.

Improving labor market conditions and lower inflation continue to support the solid streak in retail sales.

August sales were much stronger than expected, jumping 1.5%m/m after average gains of 0.8% in the preceding three months.

The inflation (H1 October) came in below expectations again at 0.46% 2w/2w, driving the annual inflation rate to yet another record low at 2.47%.

Non-core inflation drove the decline, while core inflation firmed a touch to 2.5%. With the inflation outlook bright and underlying pressures broadly absent, we expect next week's monetary policy statement to be fairly dovish.

We expect Banxico to trumpet the consolidation of lower inflation, there are other factors that favor a dovish statement overall.

A fragile global economic outlook and the recent postponement of the start of rate normalization in the U.S.

Hence, we believe the Banxico continues to stress the lack of traction in economic activity (both domestic and external), and we also believe the emphasis next week will be on lukewarm external demand and the risks embedded in the deceleration of the two biggest economies in the world.

Trade tip: MXN among few EM currency space typically held in carry basket seem cheap on a real effective exchange rate basis, Sell 3M USD/MXN call vs buy 6M 10D call.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Inflation, retail sales and external/domestic demand prompt Banxico’s conducive policy statements

Thursday, October 29, 2015 12:35 PM UTC

Editor's Picks

- Market Data

Most Popular