SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

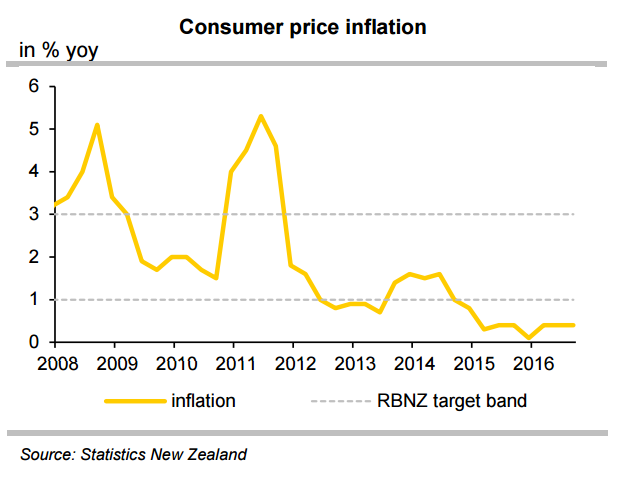

The Reserve Bank of New Zealand (RBNZ) is scheduled to hold monetary policy meeting this Thursday when it releases its Monetary Policy Statement. A great deal has changed since the RBNZ’s November Statement. The RBNZ cut the cash rate in November to a new record low of 1.75 percent and said that the policy settings including the reduction of rate would see growth robust enough to have inflation come to the middle of the target range.

Recent data has shown that New Zealand headline inflation has risen back above 1 percent in December. Headline inflation returned to the RBNZ’s target band for the first time in two years, and some measures of core inflation are back at (or close) to 2 percent. The RBNZ inflation expectations survey, released earlier today, surprised markets with a healthy jump from 1.68 percent to 1.92 percent.

The risk of expectations falling further was highlighted as a key concern in the RBNZ’s last policy statement and today's increase will have been a welcome development by the RBNZ. Increases in population and the economy’s productive capacity are allowing GDP to grow at a solid pace without a significant lift in domestic-led cost pressures. We expect these factors could impart a slightly hawkish tone to Thursday’s press release.

Speculative positioning in NZD/USD, according to CFTC futures positions of leveraged and non-commercial trader types, indicates longs are starting to be rebuilt and are at the highest level since November. A full hike is now priced in by markets by November, and certainly an OCR at record lows (and projected by the RBNZ to remain that way for the foreseeable future in November) has become harder to justify.

"We expect the RBNZ to maintain the OCR at 1.75% next Thursday, which is a view shared by the consensus and market, and strike a balanced tone. In terms of the Bank’s forecasts, we are also not expecting a major change in message." said ANZ Research in a report.

NZD/USD was trading at 0.7290 at around 1135 GMT, down 0.49 percent on the day. Price action has slipped below 5-DMA and we expect some consolidation at current levels. Major support on the downside is seen at 0.7221 (20-day MA). The longer-term trend is higher, but some near-term weakness likely on a break below 200-day MA at 0.7112.