SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market

We reckon the monetary policy divergence should be the major factor in the H2 of the year for a lower AUDUSD in the long run and interim upswings in the short run as the today’s RBA cash rates likely to remain unchanged, whereas the Fed prepares to stiffen again.

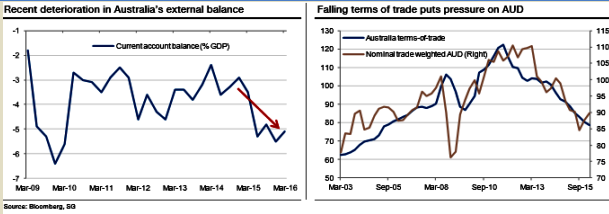

The fundamental backdrop for the Australian dollar remains challenging, though the trade-weighted AUD has fallen significantly from its highs in early 2012.

The Australian economy is gradually transitioning away from the natural resource sector, aided by low-interest rates and a weaker currency, but the current account imbalance has widened in recent quarters, non-mining CapEx growth has been elusive.

The Australian terms of trade are still falling, and thus the fundamental path of least resistance for AUD is for further depreciation (see above graph). This, plus the persistent and surprising disinflationary pressures in Australia, has kept the RBA on an easing bias, with one rate cut expected in H2 16.

The persistent weakness in nominal GDP growth has had negative consequences for government revenues, and fiscal policy should remain constrained.

While the RBA is firmly on a dovish policy setting, FX market implied volatility is elevated, Fed policy normalization remains on track and risks to the Chinese growth outlook abound (see above graph).

Australian building approvals have been massively reduced to -5.2% from the previous flash at 3.3%, while retail sales and trade balance are the data releases for the day that could add volatility to the AUD crosses in conjunction with RBA’s rate statements.

These leading economic indicators divulge economic health and how the business adopts quickly to market conditions, and their purchasing managers hold perhaps the most current and relevant insight into the company's view of the economy.

Going forward, over the longer-term, we expect AU growth to remain subpar and AUD to drift lower. There are a few key things to watch in 2016. Governor Stevens retires in Sept 2016 while the federal election results must be adding volatility to the AUD crosses. We could foresee the AUDUSD to head southwards at 0.72-0.73 by Q4 of the year.