South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

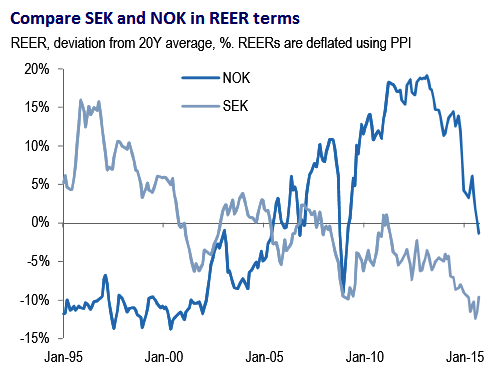

Scandinavian FX experienced the impetus of central banks resolutely pointing growth in Norway and inflation in Sweden. But the policy insertion was similar despite high Norwegian inflation and high Swedish growth.

The policy shackles should finally start to loosen for SEK next year. Growth will eliminate the output gap and core inflation should see 2% -the Riksbank's hyper-sensitivity to the exchange rate is not sustainable for a local economy that is cyclically stronger and structurally sounder than the Euro area.

EUR/SEK should eventually test the bottom of this year's 9.10-9.70 range in 2H on a late-cycle decoupling of ECB and Riksbank policy. There are limits to the Riksbank's policy of shadowing the ECB given macro divergence, as there were for the SNB.

FX weakness serves the Norges Bank's purpose in facilitating longer-term economic re-balancing irrespective of the CPI consequences. The Riksbank marginally out-did the Norges Bank (35bp of rate cuts and 5% of GDP in QE versus 50bp from the Norges Bank's) yet NOK was the harder hit, falling another 13% versus USD, 3% versus SEK and 1.5% versus EUR. NOK has now lost 36% of its value vs USD since 2013. SEK has shed 25%.

The worst real rates in G10 are a dead-weight on NOK. EUR/NOK unchanged end-2016. Expect interim upward pressure, but the peak is lowered to 9.50. End 2016 Forecasts being EUR/SEK 9.05, EUR/NOK 9.20, NOK/SEK 0.98.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Scandis currency space sensing both warmer and chilly season – SEK seems cheaper than NOK

Wednesday, February 3, 2016 10:02 AM UTC

Editor's Picks

- Market Data

Most Popular