Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

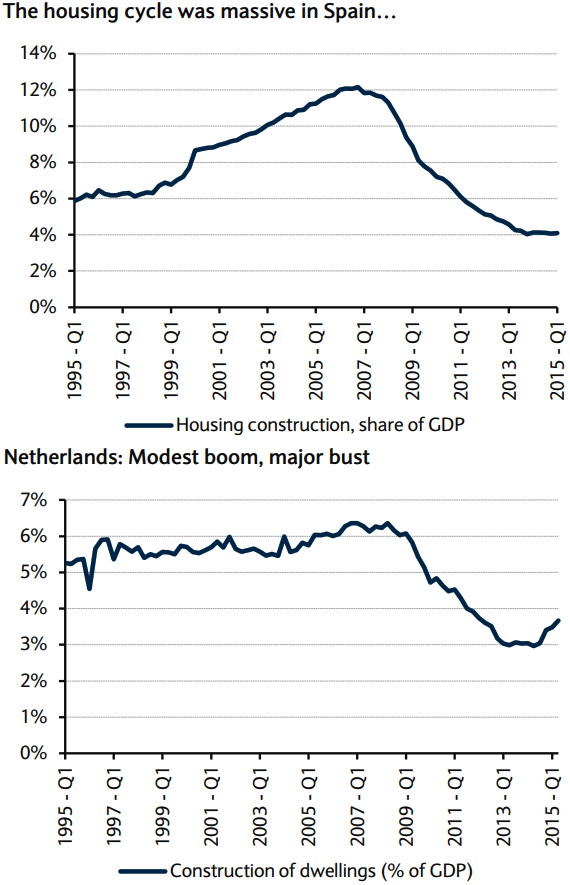

The most extreme housing booms and busts occurred in Spain and Ireland. In Spain, home construction peaked at 12% of GDP. Housing construction then fell (as percent of GDP) for 6 years in Spain, reaching historically abnormally low rates of 4% of GDP (Spain).

In contrast, some smaller countries experienced substantially more disruptive housing cycles, and these fall into at least two patterns. The Netherlands is interesting: although its construction boom was mild, it suffered a very disruptive bust. From its 2008 peak, housing construction fell for five full years, finally bottoming at 3% of GDP, roughly 2.5pp below the pre-boom norm.

This crash in home construction had more to do with a mortgage and household-debt problem than with an exaggerated episode of over-building. That said, it is consistent with evidence from other episodes that downdrafts in home construction typically last for years and the cyclical bottom is often well below historically normal rates of residential investment.

But the Spanish and Irish experiences are useful cautionary tales because they highlight just how massively the housing sector may contract after a period of overbuilding, in part because of financial pressures associated with the unwinding of the investment boom itself.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Spanish real estate failing to contribute its share of GDP – no longer an alternative avenue of investment

Thursday, September 3, 2015 7:36 AM UTC

Editor's Picks

- Market Data

Most Popular