Australia Consumer Sentiment Rises in July as Fuel Price Relief Lifts Confidence

Australia Consumer Sentiment Rises in July as Fuel Price Relief Lifts Confidence  IEA Warns China Rare Earth Export Curbs Could Threaten $6.5 Trillion in Global Production

IEA Warns China Rare Earth Export Curbs Could Threaten $6.5 Trillion in Global Production  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  Asian Currencies Stay Rangebound as Middle East Tensions, Weak China GDP Weigh on Sentiment

Asian Currencies Stay Rangebound as Middle East Tensions, Weak China GDP Weigh on Sentiment  Goldman Sees Foreign Investors Driving India Stock Market Recovery

Goldman Sees Foreign Investors Driving India Stock Market Recovery  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  South Korea’s KOSPI Enters Bear Market Despite Remaining 2026’s Best-Performing Major Stock Index

South Korea’s KOSPI Enters Bear Market Despite Remaining 2026’s Best-Performing Major Stock Index  China Home Prices Fall Again in June Despite Slower Pace of Decline

China Home Prices Fall Again in June Despite Slower Pace of Decline  Port of Los Angeles Posts Record June Cargo Volume as Importers Rush Ahead of U.S. Tariffs

Port of Los Angeles Posts Record June Cargo Volume as Importers Rush Ahead of U.S. Tariffs  Oil Prices Rise as U.S. Strikes on Iran Raise Strait of Hormuz Supply Fears

Oil Prices Rise as U.S. Strikes on Iran Raise Strait of Hormuz Supply Fears  Australian Business Conditions Hold Steady as Easing Cost Pressures Face New Oil Price Risks

Australian Business Conditions Hold Steady as Easing Cost Pressures Face New Oil Price Risks  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

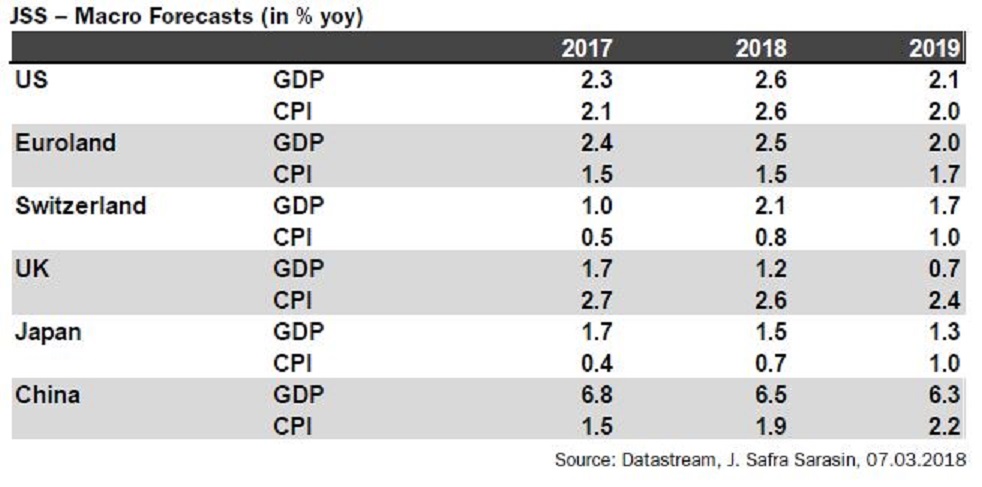

Growth remains very strong in all regions and recession risks are low even though the US-fiscal policy increases the medium-term risks of a boom-bust cycle. Main forecast revisions are that we now expect four Fed hikes in 2018, one Bank of England rate hike in May and even stronger growth rates in the eurozone and Switzerland this year. Market focus will shift to inflation developments where we are likely to have seen the trough for this year in February.

In the US, growth maintains momentum, as shown by the latest surveys of activity. Hard data suffered a partial setback at the beginning of the year, as revealed by some softness in new orders for durable goods and factory orders. Some more headwinds may temporarily result from a slowdown in personal consumption and a widening of the trade deficit.

Nonetheless, the macroeconomic fundamentals remain robust, and thanks to the further tailwinds offered by the tax cuts and the spending bill approved by the Congress, we expect solid growth in the coming quarters. On the flip side, growth momentum in conjunction with a weaker dollar and higher energy prices has the potential to fuel inflation, especially in the near term, where the base effect might lift inflation readings closer to 3 percent by the early summer.

The shifting distribution of risks surrounding inflation has been noted by the Federal Reserve; we do not envision a dramatic turn towards a more hawkish stance, but overall economic conditions clear the path for a marginally less gradual removal of monetary accommodation.

"We have increased our growth forecasts for the euro area to 2.5 percent in 2018 and 2.0 percent in 2019 and the Swiss forecast to 2.1 percent this year. Labour markets improve in both currency areas and lay the ground for higher consumer confidence, stronger private consumption, and higher wage increases. As an example, the unemployment rate fell to 2.9 percent in Switzerland – a level lower than end 2014 before the discontinuation of the currency-floor", the report added.

Finally, the ECB decided to get rid of its easing bias in its policy statement. Given the scarcity of government bonds, strong growth, tight credit spreads and somewhat increasing inflation rates this move can be easily justified. It was not necessarily expected by markets to take place at the meeting this month but implies that the ECB will be under less pressure to adjust its communication at the April meeting.

Lastly, FxWirePro has launched Absolute Return Managed Program. For more details, visit http://www.fxwirepro.com/invest