Japan Signals Readiness to Act on Yen as Intervention Speculation Grows

Japan Signals Readiness to Act on Yen as Intervention Speculation Grows  Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations

Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations  U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk

U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk  Moody’s Says Peru’s President-Elect Keiko Fujimori Could Boost Investor Confidence

Moody’s Says Peru’s President-Elect Keiko Fujimori Could Boost Investor Confidence  Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens

Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens  Oil Prices Slip as Oversupply Concerns and U.S.-Iran Talks Shape Market Outlook

Oil Prices Slip as Oversupply Concerns and U.S.-Iran Talks Shape Market Outlook  Brazil to Phase Out Gasoline Subsidy First as Diesel Support Stays Longer

Brazil to Phase Out Gasoline Subsidy First as Diesel Support Stays Longer  Asian Currencies Rise as Dollar Weakens; Yen Holds Steady Amid Japan Intervention Watch

Asian Currencies Rise as Dollar Weakens; Yen Holds Steady Amid Japan Intervention Watch  Gold Price Rises as Softer Dollar and Fed Rate Expectations Boost Bullion Demand

Gold Price Rises as Softer Dollar and Fed Rate Expectations Boost Bullion Demand  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions

Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions  Iran Begins Oil Sale Talks With Japan Under U.S. Sanctions Waiver Amid Shipping Risks

Iran Begins Oil Sale Talks With Japan Under U.S. Sanctions Waiver Amid Shipping Risks  Asian Markets Slip as AI Earnings Season Looms, Oil Prices Fall Ahead of Key Fed Signals

Asian Markets Slip as AI Earnings Season Looms, Oil Prices Fall Ahead of Key Fed Signals  China Services PMI Beats Forecasts as Strong Demand Supports June Growth

China Services PMI Beats Forecasts as Strong Demand Supports June Growth  Wall Street Ends Mixed as Weak Jobs Data Lowers Fed Rate Hike Bets, Chip Stocks Tumble

Wall Street Ends Mixed as Weak Jobs Data Lowers Fed Rate Hike Bets, Chip Stocks Tumble  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Two key factors distinguish the economic consequences of coronavirus from those of previous crises. One is the catastrophic decline in employment in such a short space of time. The other is the incredibly swift digital transformation which has changed the way society works and consumes.

In this new digital landscape, as well as a widespread shift to home working, the resurgence of e-commerce and even the remote provision of healthcare have become facts of everyday life. In effect, the credit for the rapid digitising of most companies does not belong with business leaders – but to the arrival of Covid-19.

Any exit from the current lockdown is likely to reverse some of this digital transformation, but not all of it. And the unprecedented scale of what has happened will have a significant impact on employment levels for a long time – even as economies rebuild.

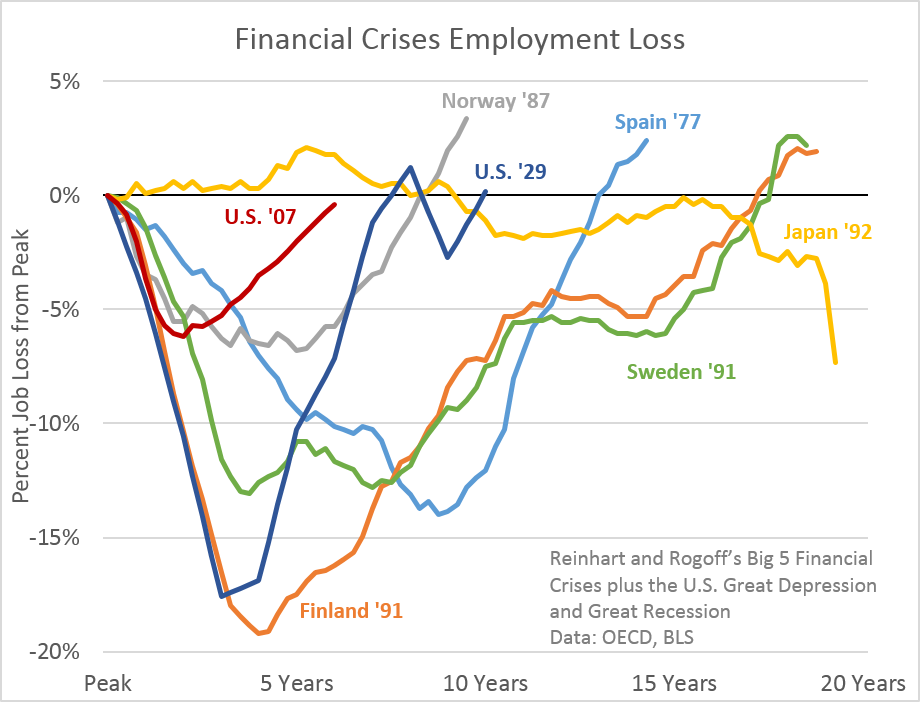

Indeed, weak employment growth has been a key feature of previous economic recoveries – a phenomenon economists call “jobless recovery”. In the US, following the global financial crisis of 2008, it took over six years for employment to get back to its pre-recession peak. The recessions of 1991 (after the Gulf War) and 2001 (the dot-com bubble crash), also saw long-lasting high levels of unemployment, with immense economic and social consequences.

In Europe, the effect on employment after 2008 was even more dramatic. It took the EU 11 years to return to its pre-crisis unemployment rate of 6.7%.

Recovery without jobs

Put simply, these jobless recoveries were caused by a mixture of globalisation and digitisation. Essentially, manufacturing jobs end up moving from advanced economies to destinations offering cheap labour, while advances in technology replace labour.

The vast scale of the digital transformation caused by coronavirus is likely to make any recovery even more jobless than in the past.

This leaves politicians with the difficult task of formulating policies that will counteract these unfavourable effects. They will need to come up with a plan that reverses the contraction in economic activity, reduces income inequality (or at least doesn’t worsen it and minimises impact on government debt.

On that final point, it is worth mentioning that in the UK, national debt as a percentage of income is forecast to edge towards 100% – although some believe it be even higher. This figure was 75% in 2010 – and widely seen as unsustainable.

Our recent research has shown that there are trade-offs among these three objectives. For example, policies which stimulate the economy and reduce government debt often benefit business owners at the (relative) expense of workers. But policies which help the poorer in society have less of an impact on government debt as these households contribute less tax.

We also found that higher spending and lower taxes are particularly effective in economic downturns. This is because households tend to spend any additional earnings, helping the economy to bounce back faster.

Also, when interest rates are at record low levels, there is a potential for what we call “fiscal free lunches”. That is, tax cuts could raise income to such an extent that the additional tax revenue generated more than pays for any initial rise in government expenditure.

So policy looking to minimise the potential for a jobless recovery should look to increase production in the economy and increase the marginal returns from hiring labour.

For example, cuts to corporate tax rates can help by improving business profits, although cuts to employers’ national insurance contributions would be a more effective approach to directly addressing employment levels.

Also, while corporate tax cuts might end up increasing income inequality (by increasing dividends for shareholders) reducing national insurance contributions would increase demand for labour, raising both employment and wages. The government could also look to accelerate infrastructure spending, improving the productive capacity of the economy and providing a spending stimulus which targets long-term results.

Overall, the most significant impact on the economy and employment would come from a complete structural reform to tax and spending policy. In 2011 a comprehensive review of UK tax structure highlighted many inconsistencies and inefficiencies, concluding that the system was “inefficient, overly complex and frequently unfair”.

Since then, some small changes have been made, but these inefficiencies and complexities persist. If there was ever a good time to initiate truly bold reforms, it is now.

The authors do not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.

The authors do not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.

{kind=link}

{kind=link}