BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation

RBA maintains status quo to leave its cash rates unchanged at 1.50%, our outlook on the Aussie central bank is to remain on hold throughout 2018, and this is anchoring short-maturity interest rates and should keep 3y swap rates in a 1.80% to 2.30% range, as long as core inflation remains below 2%. Longer maturity rates will largely follow US rates.

Stay long EURAUD and EURNZD as de-synchronized central bank policy cycles, sensitivity to protectionism-inspired risk market stress and medium term valuations continue to underpin our constructive stance on EURAUD and EURNZD.

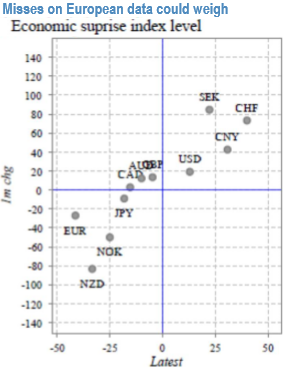

We would have preferred to see a more forceful de-coupling of the Euro from the commodity bloc as trade anxieties mounted this week, but were frustrated by the co-incidence of weaker-than-expected European PMIs. The downward inflection in the European data cycle, albeit at impressively high activity levels, bears close watching as a tactical risk to EUR longs.

Negative data surprises (refer 1st chart) have forced our economists to lower their sights on 2Q’18 growth from 3% to 2.5% QoQ SAAR and pencil in a short taper in 4Q’18 instead of QE ending in September as earlier envisioned.

EUR now features as a sell within our rule-based economic momentum framework as a result of this forecast revision and some trimming of heavy spec longs in the near-term should not come as a surprise.

For EURAUD and EURNZD, the offset is that antipodean data and policy developments over the past two weeks did little to persuade us that shorts in these currencies require a re-think. In Australia, a weak labor market report re-highlighted risks to an over-leveraged household sector, and RBA minutes appeared to edge lower its views on potential growth in a continuation of the slightly dovish strain of commentary from the Bank in recent weeks.

In New Zealand, the 4Q real GDP print came in below consensus expectations and was explicitly noted in this week’s RBNZ statement.

Growth appears to have peaked for the cycle and is likely to fall short of the RBNZ’s +3% forecasts.

Policy rates in both countries, particularly Australia, have substantial room to fall to re-align with the serial disappointment in real activity in recent months (refer 2nd chart); our core thesis is that this should increasingly exert a greater influence on exchange rates as G3 central banks lift rates further and/or move closer to normalization.

A dovish leaning revision of Fed dots in the March SEP and European data misses may have delayed but not canceled the intensification of these rate pressures.

Buy EURAUD spot trades at 1.5880, stop at 1.5575. Marked at +0.47%.

Add longs in a 9m 1.80 EURNZD AED call with a 3m 1.80 window KO. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: