Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

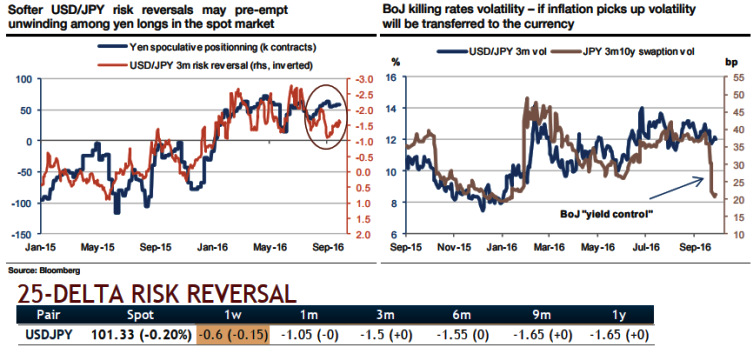

Since the beginning of last year, US long rates have again become the main USDJPY driver. The BoJ’s peg on JGB yields is going to kill yen rates volatility so that the rates factor should become even more US-centric.

But the mild Treasuries sell-off right after that, which saw 10y yields briefly trading below 1.40%, was not enough to lift the US dollar. At the same time, the FX market challenged the BoJ, so that USD/JPY and the US yields diverged. Lagging US yields – a catch-up would imply a move above 105.

This correlation is notably unstable, but the mean-reversion between FX and rates has been powerful over recent years. US rates are now unlikely to drift much lower and should not precipitate a USDJPY break, meaning a catch-up higher is a more likely scenario. The current relationship suggests a move above 105.

Softer options positioning may pre-empt an unwinding of yen longs:

Positioning in spot and options markets tends to evolve in tandem, even if options investors are expressing views with a conditional nature.

Since the CFTC records futures positions, the current long yen positioning has only been matched by the 2008 peak reached when Bear Stearns collapsed.

Such an extreme positioning is hardly sustainable, and the softer skew in yen options markets might be sending the signal that longs are eroding (the 3m risk reversal is decoupling from futures positions – see above nutshell and graph).

On top of that, OPEC’s surprise announcement of production cuts is supporting risky assets, instating a risk-friendly environment (higher stocks and commodities), which should further discourage yen longs.