Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets

Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks  Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening  Trump Questions USMCA Renewal as Trade Talks Continue

Trump Questions USMCA Renewal as Trade Talks Continue  US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook

US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook  Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict

Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict  Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge  Dollar Surges After Fed Holds Rates Steady, Signals Potential Tightening Ahead

Dollar Surges After Fed Holds Rates Steady, Signals Potential Tightening Ahead  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

In H2, we expect AU growth to remain subpar and AUD to drift lower. There are a few key things to watch in 2016. Governor Stevens retires in Sept 2016 while a federal election must be held tomorrow; opinion polls are fairly evenly balanced, although betting markets suggest a Liberal-National Coalition win.

The shock Brexit result is likely to be an important part of the policy deliberations when the RBA Board meets on next Thursday, while AU’s current account deficit is also worth tracking.

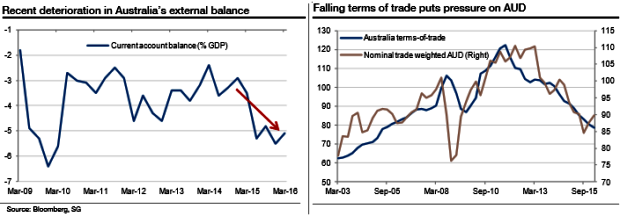

The fundamental backdrop for the Australian dollar remains challenging, though the trade-weighted AUD has fallen significantly from its highs in early 2012. The Australian economy is gradually transitioning away from the natural resource sector, aided by low-interest rates and a weaker currency.

But the current account imbalance has widened in recent quarters, non-mining CapEx growth has been elusive, the RBA is firmly on a dovish policy setting, the above chart shows that FX market implied volatility is elevated, Fed policy normalisation remains on track and risks to the Chinese growth outlook abound.

The Australian terms of trade are still falling, and thus the fundamental path of least resistance for AUD is for further depreciation. This, plus the persistent and surprising disinflationary pressures in Australia, has kept the RBA on an easing bias, with one rate cut expected in H2 16. Monetary divergence should thus be another factor in the second half of the year for a lower AUD/USD as the Fed readies to tighten again.

The persistent weakness in nominal GDP growth has had negative consequences for government revenues, and fiscal policy should remain constrained. The opposition Labour Party has committed itself to fiscal consolidation to preserve Australia’s AAA credit rating. There is thus unlikely to be significant changes to fiscal policy whatever the outcome of the July 2016 general elections.

Moreover, global macro uncertainty has buoyed global FX implied volatility. This has historically been a negative factor for AUD and we expect it to remain so. While we do see further weakness in AUD through H2 16, it should be at a more gradual pace given the sizeable valuation mean-reversion that has already occurred. But we do see value emerging in the AUD/NZD cross at current levels.