Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  US Yen Intervention Unlikely to Deliver Lasting Recovery, Yardeni Says

US Yen Intervention Unlikely to Deliver Lasting Recovery, Yardeni Says  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Yen Stabilizes After Intervention Slide as Australian Dollar Hits Eight-Week High

Yen Stabilizes After Intervention Slide as Australian Dollar Hits Eight-Week High  Oil Prices Rise as Hormuz Reopening Remains Uncertain

Oil Prices Rise as Hormuz Reopening Remains Uncertain  Japan Posts First Current Account Deficit in 17 Months as Dividend Payments Surge

Japan Posts First Current Account Deficit in 17 Months as Dividend Payments Surge  BOJ Signals Faster Rate Hikes as Inflation Risks Raise September Move Odds

BOJ Signals Faster Rate Hikes as Inflation Risks Raise September Move Odds  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Asian Stocks Rise as Weak US Jobs Data Eases Fed Rate Hike Fears

Asian Stocks Rise as Weak US Jobs Data Eases Fed Rate Hike Fears  Japan Executives Warn Weak Yen and Currency Volatility Threaten Economy

Japan Executives Warn Weak Yen and Currency Volatility Threaten Economy  Gold Prices Hold Near Seven-Week High as Markets Await U.S. Inflation Data

Gold Prices Hold Near Seven-Week High as Markets Await U.S. Inflation Data  Gold Prices Rise as Fed Rate Hike Bets Ease

Gold Prices Rise as Fed Rate Hike Bets Ease  S&P 500, Nasdaq Slip as Oil Jumps on Iran Tensions

S&P 500, Nasdaq Slip as Oil Jumps on Iran Tensions  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

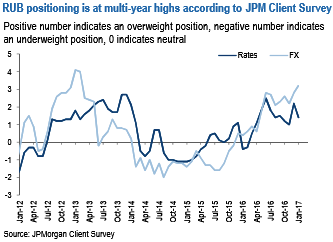

Every good structural story needs a repricing and a clear-out of extended positioning. The medium-term case for Russian local markets is underpinned by high nominal and real interest rates, falling inflation, and a trend of improving macro policy credibility. Yet investors are already positioned to be very long and valuations are only beginning to correct from a starting point of overvaluation (refer above graphs).

In this context, the decision of the CBR to intervene in the FX markets to the tune of $2bn per month is a catalyst for positioning to wash out and a repricing of Russian local rates and currency assets in the short term.

The FX intervention program will be a meaningful drag on the BoP. To put this into perspective, the currently estimated $23bn FX intervention in 2017 compares to our $33bn current account surplus forecast for the year.

The 2015 FX reserve accumulation program resulted in at least 5% RUB depreciation. This is based on the RUB depreciation over the period adjusted for movements in oil and CDS prices.

RUB is overvalued. In our short term FX model, RUB entered the FX intervention announcement trading 2% rich to oil. This has now been corrected to a flat position but we still expect the currency to have to start trading cheap to oil. In our long term REER model, RUB is 5% rich.

RUB positioning is extended. RUB is now the second most extended long globally after BRL.

Oil positioning is extended. Net longs in crude are at their highest levels since mid-2014 increasing risks for a correction. While the new intervention policy should eventually limit RUB’s sensitivity to oil, this will only be the case once RUB reaches its new equilibrium. From current levels, we believe oil price correction is a complementary risk.

To express this view of short-term risks pointing to a repricing and clearing out of long positions, we recommend the following trade: Go long USDRUB with a 63.5 target and 58.5 review level.