BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

The OCR is biased lower, but like the consensus and market, we don’t expect action at the OCR Review on Thursday. Further easing will be signalled – the NZD is too deflationary to ignore, and doing nothing would send it further skyward – but the RBNZ has shown a preference to move on Monetary Policy Statement dates.

We remain in an environment where conventional policy signals (growth, output gap, housing, capacity) are flagging no change (or hike!), but they are going head-to-head with factors that are by-and-large beyond the RBNZ’s control (global scene, NZD) amidst some concerns over consistently low inflation influencing price-setting behaviour.

The environment needs pragmatism, balance, and measured messages. We expect further policy easing to be signalled, leaving the door well and truly open to a November cut. The strong NZD will continue to “make it difficult for the Bank to meet its inflation objective”. That highlights the direction of risk for the OCR. We suspect that the 35bps of additional OCR cuts signalled in the August MPS are still more-or-less the RBNZ’s base case. And that is broadly consistent with current market pricing.

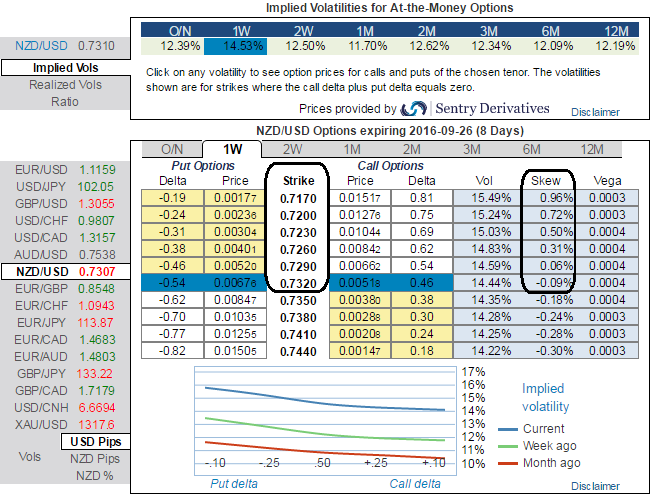

FX Option Outlook:

Although the NZ dollar edged higher against its U.S. counterpart during early Asian trading sessions and 1w implied volatilities are flashing shy above 14.5% ahead of above mentioned RBNZ’s monetary policy season, IV skewness signifies the OTC interest in OTM put strikes.

Hence, if you want to write calls, OTM call options instead of ATM calls are deemed the right choice in prevailing bearish environment.

Expensive implied volatility and spot within a channel Implied volatility is elevated compared to realized volatility, suggesting a structure selling it.

The downside skew is not sufficiently elevated to finance a put via low strikes (a put spread-like structure), but the negative skew is enough to obtain an attractive discount via a downside knock-out.

Such a barrier is appropriate for trading moderate NZDUSD downside, keeping in mind that the spot has been trapped within a bullish channel since the start of the year and that 0.70 is below the support line.

Hence, we think call writing could also be beneficial as IV skewness is conducive for prevailing bearish environment.