Seagate Stock Jumps as AI-Fueled Earnings Beat and Strong FY2027 Outlook Impress Investors

Seagate Stock Jumps as AI-Fueled Earnings Beat and Strong FY2027 Outlook Impress Investors  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Meta CEO Zuckerberg Opposes U.S. Ban on Chinese AI Models, Warns Against Overregulation

Meta CEO Zuckerberg Opposes U.S. Ban on Chinese AI Models, Warns Against Overregulation  Arm Holdings Q1 Earnings Beat Estimates, Strong Q2 Outlook Fails to Lift ARM Stock

Arm Holdings Q1 Earnings Beat Estimates, Strong Q2 Outlook Fails to Lift ARM Stock  Robinhood Q2 Earnings Beat Estimates, But HOOD Stock Falls as Investors Question Profit Quality

Robinhood Q2 Earnings Beat Estimates, But HOOD Stock Falls as Investors Question Profit Quality  Chipotle Q2 Earnings Beat Expectations as Sales Growth Drives Higher 2026 Outlook

Chipotle Q2 Earnings Beat Expectations as Sales Growth Drives Higher 2026 Outlook  Sika Raises 2026 Sales Outlook After Strong First-Half Results Beat Expectations

Sika Raises 2026 Sales Outlook After Strong First-Half Results Beat Expectations  Barclays Q2 Profit Beats Forecasts as Investment Banking Strength Offsets Higher Costs

Barclays Q2 Profit Beats Forecasts as Investment Banking Strength Offsets Higher Costs  Exosens H1 Profit Beats Forecasts as Defense Demand Drives Growth

Exosens H1 Profit Beats Forecasts as Defense Demand Drives Growth  Toyota First-Half Global Sales and Production Decline on Weak China Demand, RAV4 Transition

Toyota First-Half Global Sales and Production Decline on Weak China Demand, RAV4 Transition  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Rio Tinto Stock Jumps as Strong Earnings, Higher Dividend and AI Metal Demand Boost Outlook

Rio Tinto Stock Jumps as Strong Earnings, Higher Dividend and AI Metal Demand Boost Outlook  OpenAI Revenue Surges After GPT-5.6 Launch as IPO Expectations Grow

OpenAI Revenue Surges After GPT-5.6 Launch as IPO Expectations Grow  TSMC Gradually Restarts Japan Chip Plant After Kumamoto Earthquake

TSMC Gradually Restarts Japan Chip Plant After Kumamoto Earthquake  GSK Unveils $2.52 Billion Cost-Cutting Plan to Accelerate Drug Pipeline

GSK Unveils $2.52 Billion Cost-Cutting Plan to Accelerate Drug Pipeline  Sony Eyes $1.3 Billion Tamron Acquisition as Lens Maker Reviews Offer

Sony Eyes $1.3 Billion Tamron Acquisition as Lens Maker Reviews Offer  Samsung Q2 Profit Surges on AI Memory Chip Demand, Forecasts Strong Second Half

Samsung Q2 Profit Surges on AI Memory Chip Demand, Forecasts Strong Second Half

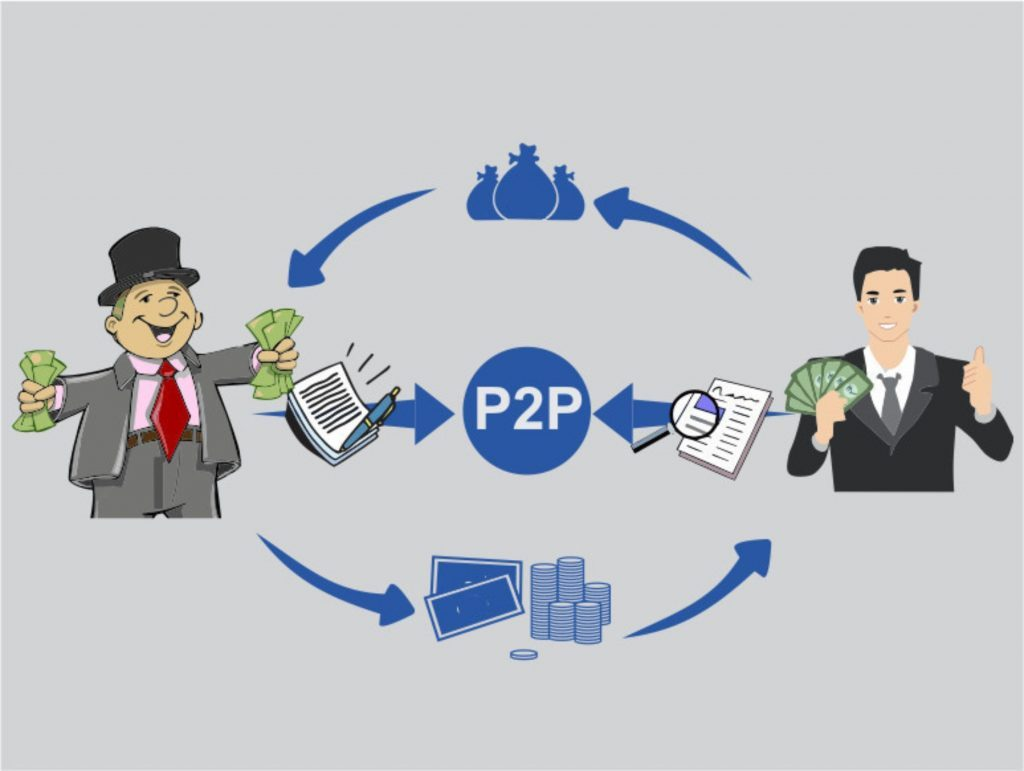

P2p lending is a method of financial transactions in which money is borrowed without the participation of banks. And the lender is not a corporation but an individual. The abbreviation p2p stands for peer-to-peer. Another decryption option is Person-to-Person.

The Essence of Mutual Lending

Lending venues are p2p lending sites. A person is registered there as a borrower or lender, after which he can take or give loans. The exchange is not a creditor, but it plays an important role, acting as an intermediary in transactions and checking the reliability and solvency of borrowers.

Despite the outward simplicity of conducting operations, the p2p service involves studying the credit history of borrowers and creating a confidence rating to reduce investor risks. Relations between the lender and the borrower are held together in a contractual format. The contract has legal force and can be used as confirmation in the course of litigation. But it rarely comes to trial.

The attractiveness of this credit system is that it is beneficial for both parties. The percentage of the lender’s return on investments in p2p is higher than the percentage on bank deposits. And the borrower can quickly take small amounts of money for the short term, passing a less stringent check of his reliability.

Risks and Weaknesses

P2p lending has the following risks:

- Since the contact of the lender and the borrower passes only through the Internet, it is easier for the latter to hide with the money received and not return it.

- Although exchanges test users for reliability, their degree of control is not as great as in banks. Often, citizens with a negative credit history are allowed to register.

- Automated verification and rating systems are easily fooled by an experienced scammer. Counterfeit documents, fake accounts, and other methods can go into business.

- Fraudsters practice this way of earning. For example, the user takes and timely returns several inexpensive loans. This allows him to get a high rating, with the help of which he receives expensive loans on favorable terms and does not return them. Exchanges try to fight this scheme in different ways.

- Many sites do not work with bank transfers, but with electronic money, the circulation of which is regulated and protected not so strictly.

Reviews

Although p2p lending is described by some publications as a replacement for the banking system, most Internet users are more skeptical. The opacity of Internet schemes, the relatively low amount of investment, and the lack of full-fledged functionality of large financial organizations do not allow p2p to be perceived as a complete alternative to classical banking.

This is a niche industry. But within its niche, this system has the right to live. In such areas as small consumer lending, financing of small businesses and start-ups, and urgent loans for urgent needs, the p2p system is doing well and has bright prospects for further development.

This article does not necessarily reflect the opinions of the editors or management of EconoTimes.