US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention

Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict

Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade

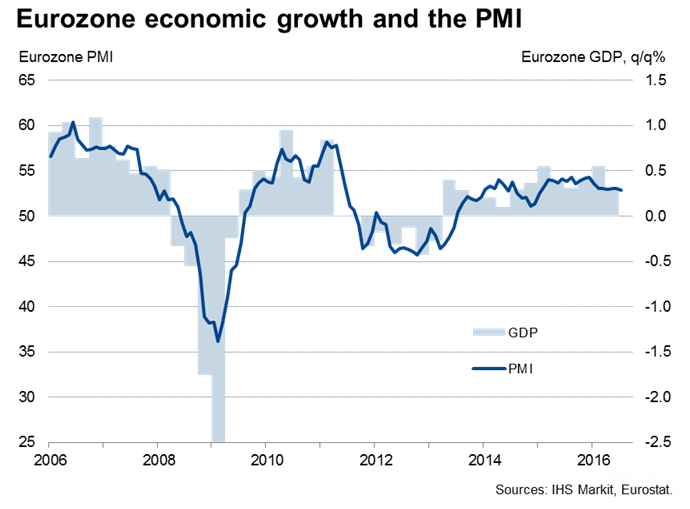

According to the preliminary estimates released on Friday, the Euro area recorded a tepid economic growth of 0.3 percent q/q in the second quarter of 2016. The reading was in line with market expectations but was well short of 0.6 percent q/q growth recorded in the previous quarter.

After the strong growth in the first quarter which was helped by some temporary factors like the mild winter weather, some pay-back in the second quarter was expected. On a yearly basis, eurozone GDP was up 1.6 percent, slightly less than the upwardly revised 1.7 percent recorded in the first quarter.

French statistics office released GDP data earlier on Friday which showed growth of the euro zone's second-largest came in at a worse-than-expected at zero due to weak consumer spending. The disappointing zero percent growth in France, largely due to a decline in inventories, was one of the culprits behind the weaker Eurozone growth performance.

It is worth noting that today’s release refers to economic growth in the three months to June, ahead of the UK’s vote to leave the EU. Also, GDP figures for big member states comprising Germany and Italy still have to be published, implying that today’s figure is prone to revision.

"Risks of a downward revision to these data are high. The great unknown is German GDP, and more specifically capital expenditure in the construction industry," said Claus Vistesen at Pantheon.

In a separate report, the eurozone flash HICP inflation estimate showed that headline inflation came out at 0.2 percent in July, slightly higher than expected 0.1 percent. The reading which was its highest since the end of last year was driven by food, alcohol and tobacco. Today’s set of data gives policy makers only limited comfort as inflation remains uncomfortably low.

"The case for the ECB to announce further policy easing in September will continue to strengthen. We have pencilled in a cut to the deposit rate from -0.4 percent to -0.5 percent and an increase in the monthly pace of asset purchases from €80bn to €90bn." said Nick Kounis at ABN Amro.

The common currency keeps the firm footing at the end of the week post-EMU data. EUR/USD advanced further to hit highs of 1.1114 and was trading at 1.1110 at 11:30 GMT, while EUR/GBP was trading at 0.8430.