China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  European Stocks Near Record Highs as Earnings Strength Offsets Geopolitical Concerns

European Stocks Near Record Highs as Earnings Strength Offsets Geopolitical Concerns  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  Gold Price Hits Seven-Week High as Fed Rate Hike Bets Fade and Hormuz Deal Hopes Grow

Gold Price Hits Seven-Week High as Fed Rate Hike Bets Fade and Hormuz Deal Hopes Grow  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  China Trade Surplus Beats Forecasts in July as Exports Stay Strong

China Trade Surplus Beats Forecasts in July as Exports Stay Strong  US Stock Futures Rise as Markets Await July Payrolls Data

US Stock Futures Rise as Markets Await July Payrolls Data  Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns

Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns  Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness

Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness  Singapore Says One-Third of U.S. Exports Hit by New 12.5% Tariff

Singapore Says One-Third of U.S. Exports Hit by New 12.5% Tariff  Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data  Asian Currencies Steady as Markets Await U.S. Jobs Data

Asian Currencies Steady as Markets Await U.S. Jobs Data  European Natural Gas Prices Hold Near Three-Week Lows Amid Middle East Talks and Supply Concerns

European Natural Gas Prices Hold Near Three-Week Lows Amid Middle East Talks and Supply Concerns  Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes

Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes  Oil Prices Surge as Iran Hormuz Restrictions Renew Supply Fears

Oil Prices Surge as Iran Hormuz Restrictions Renew Supply Fears  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Asian Currencies Hold Steady as US Dollar Nears Seven-Week Low Ahead of Key Jobs Data

Asian Currencies Hold Steady as US Dollar Nears Seven-Week Low Ahead of Key Jobs Data

The COVID-19 pandemic has seriously disrupted the UK economy and major increases in unemployment are already occurring. It has already been reported that 649,000 jobs have disappeared during the lockdown.

If history tells us anything, it’s that a significant surge in unemployment could cost Boris Johnson significant voter support – and even the next election.

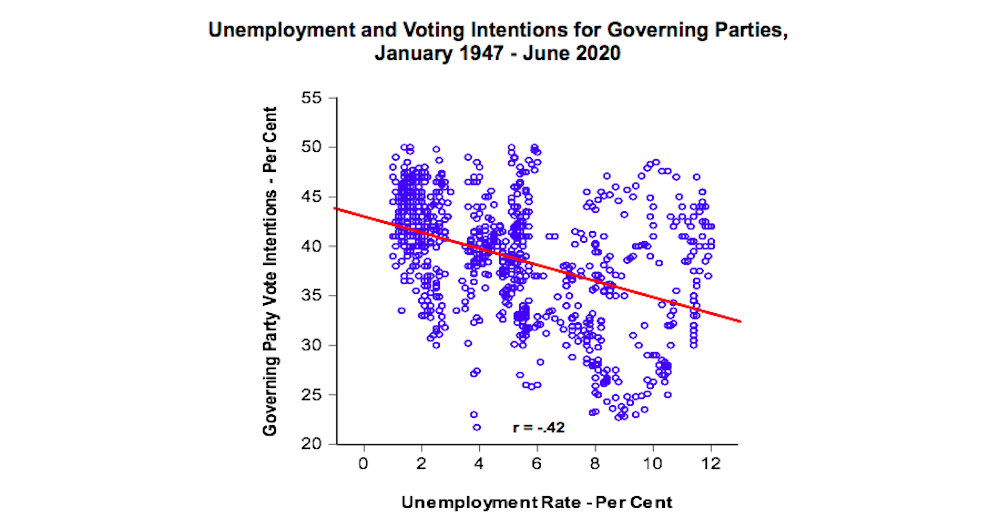

The chart below uses monthly polling data to show the relationship between the unemployment rate and voting intentions for the governing party from January 1947 to June 2020. Each dot represents a poll and the fitted values line shows the average relationship between the two variables over this 73-year period.

The figure displays government voting intentions up to a ceiling of 50%, but occasionally it has been higher than that, for example, when Tony Blair’s government achieved 60% just after Labour’s landslide victory in the 1997 general election. But since no governing party has won more than 50% of the vote in elections since the second world war, we examine a feasible range of possibilities.

What history tells us. Author provided

The polls are widely scattered, but there is nonetheless a sizeable and highly statistically significant correlation between the two measures of -0.42 (on a scale ranging from 0 to +/-1.0). As the red summary (fitted values) line shows, this means that when unemployment rises, public support for the governing party falls.

This long-run historical relationship is important because the UK is about to see unemployment rise to levels not seen for a generation. In the December 2019 election, the Conservatives won nearly 44% of the vote when UK unemployment was 3.9%. At that time, the rate of joblessness had been falling for six years, and this created a quite benign economic environment for an incumbent party to fight an election.

Additional modelling of these relationships considers the effect on changes in unemployment on voting intentions for the governing party a month later. The numbers indicate that when unemployment increases by 1%, this will reduce the change in voting intentions for the governing party by just over 1% in the following month. When unemployment goes up, governing party support goes down.

To be fair, it is very unusual for unemployment to increase by that amount in a single month. In normal times joblessness is subject to a lot of inertia. That said, the number of people claiming unemployment benefits increased by more than half a million in May this year to a total of 2.8 million people. As the COVID-19 crisis became increasingly serious between March and May, the claimant count grew by 1.6 million. That is an unprecedented jump in joblessness over the entire period since the end of the second world war.

Until now, rising unemployment has not had much an impact on support for the government. A Deltapoll conducted in early July put the Conservatives on 44%, which is almost exactly what they received in the general election last December. The big news is that Labour is now on 38%, having taken only a 32% vote share in the election.

These poll numbers show that the well-established relationship between unemployment and government support has not yet kicked in, but there are good reasons why this is the case. The first is that the COVID-19 pandemic is an unprecedented event by any standards and most voters understand this fact. Moreover, there was considerable public support for locking down the economy, which of course has led to massive numbers of people losing their jobs. The government clearly cannot be blamed for this state of affairs.

The second is that the government has provided unprecedented largesse in supporting jobs with the furlough scheme. This has been popular and thus far has prevented unemployment from getting even worse.

The problem will come, however, when the immediate impact of the COVID-19 crisis starts to fade as people return to a semblance of their normal lives and, above all, when the furlough scheme comes to an end in October. This is when the true political costs of the jobs crisis will start to be felt. If so, eventually we are likely to return to the normal relationship between unemployment and support for the governing party.

Given this, let’s suppose that unemployment reaches 12% within the next year or two – something which actually happened in early 1984 as a result of Margaret Thatcher’s austerity policies. The chart above suggests that this rate of joblessness would put governing party voting intentions at between 32% and 33%. This estimate is, of course, subject to considerable uncertainty, but with Labour now moving up in the polls this could easily sink the government in the 2024 election.

The next general election is a long way off, but history tells us that large increases in unemployment will make life difficult for Johnson in the months ahead.