U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

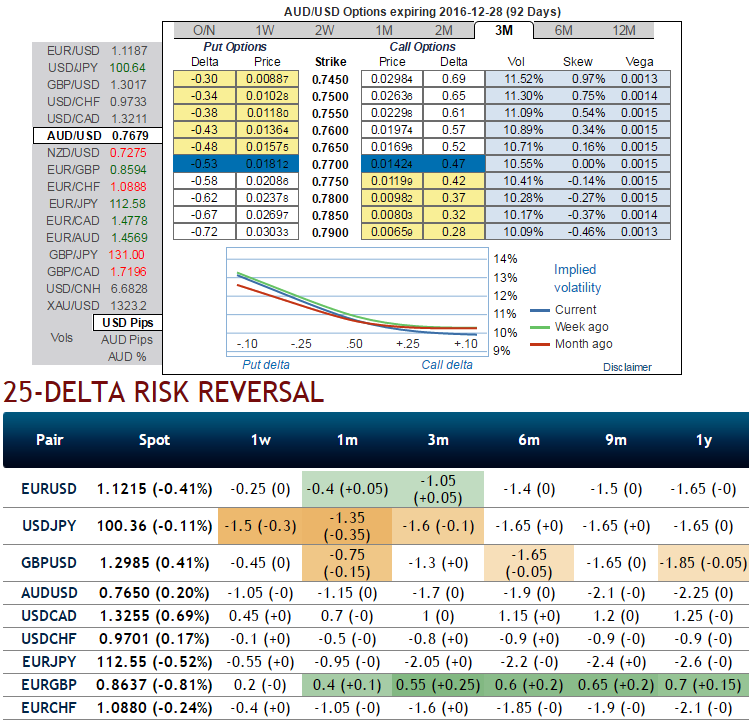

Please be noted that the skewness in implied volatility of 3m tenors of this pair signifies the hedgers interest in OTM put strikes.

While delta risk reversals of the similar expiries reveal more sentiments in hedging activities for downside risks. This would raise a cause of concern that in this phase of time, the major economic events are likely to intensify volatility in FX markets.

Hence, we could foresee AUDUSD’s direction below 0.72 in the months to come, given:

(1) The RBA easing cycle becomes more aggressive, as domestic growth slips;

(2) China growth forecasts are cut materially, or the pace of slowing accelerates; or

(3) The carry trade unwinds in response to a rise in G3 bond yields.

(4) A retracement in commodity prices should cap AUDUSD.

(5) Hopes on Fed’s rate hike during December.

Monetary policy drivers take a back seat for AUD in coming months. With the RBA now on hold for the remainder of 2016 (having cut rates by 50bp in Q2/Q3 in response to an inflation shock).

The Fed likely to be on hold until late in Q4 once money market reforms and the Presidential election are out of the way, it is hard to argue that monetary policy expectations will have much of an effect on AUDUSD in coming months.

Indeed, the recent compression in front end rate differentials as the RBA has cut rates has had little impact on AUDUSD of late, suggesting that the level of front end rates – and expectations about the path of front end rates – have had less influence on AUD than historical experience would suggest.

Contemplating the above fundamental as well as OTC factors, we construct strategy comprising of both calls as well as puts in the ratio of 3:1 so as to suit the swings on either directions.

Capitalizing on lower IVs we eye on shorting at the money calls with shorter expiries which would lock in certain yields by initial receipts of premiums and risk reversals to favour longs in puts in lengthier tenors.

Well, here goes the strategy, go short in 1m OTM calls and simultaneously, 3 lots of 3m puts (+1% ITM, ATM and +1% OTM strikes) are preferred to suit the prevailing losing streaks. So thereby the combination would be executed for net debit and the cost is reduced by short side.

Moreover, the strategy could be counterproductive as the skews in 3m IVs favours OTM puts strikes.