Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

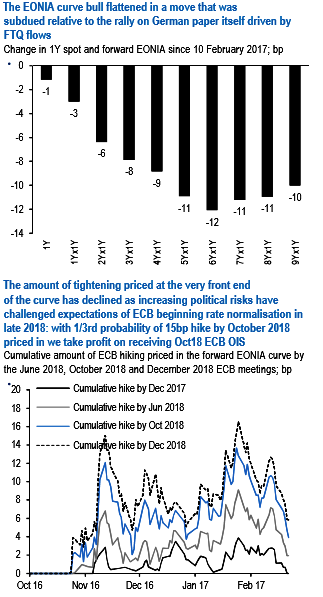

The EONIA curve bull flattened with a notable outperformance of post 5Y forwards (refer above diagram). The dynamic was different relative to the German curve, where the large outperformance of Schatz led to bull steepening of the German curve. Flight-to-quality flows on increasing concerns on French political risks were the main drivers.

The amount of tightening priced at the very front end of the curve has declined as increasing political risks have challenged expectations of ECB rate normalization in late 2018. We still believe that the ECB will increase policy rates 6M after the end of QE purchases which we expect at June 2018. With the market now pricing about 1/3rd probability of a 15 bp hike in the deposit rate by October 2018 (refer above diagram), we take profit on receiving Oct18 ECB OIS.

After the recent rally greens EONIA are now priced fully in line with our risk scenario of ECB starting to hike rates in late 2019 limiting the attractiveness of long positions in the sub 3Y sector (refer above diagram). Further out we are still biased for a steeper money market curve but we acknowledge that the political risks are going to limit the rate normalization priced in by the ECB, given the risk scenario of a Le Pen Presidency and potential EMU/EU referendum.

We prefer to hold steepening exposure in the money market curve via conditional structures. Specifically, we hold reds/blues weighted swap curve conditional steepener via 3M midcurve payers. The weighted curve continues to remain strongly directional and is currently trading too flat vs. yield levels (refer above diagram).

Two weeks ago we recommended conditional bull flattener to hedge against the risk of further FTQ driven rally combining the bull flattening view of the swap curve (1s/5s) with the bull widening view in Bobl swap spreads. Over the period the swap curve the bull flattened and Bobl swap spreads widened 8bp (refer above diagram). Thus we tactically take profit on 1Y swap/Jun17 Bobl conditional bull flattener. The richening of Bobl implied volatility has reduced the attractiveness of this conditional structure, with 3Mx1Y implied now priced at about 20-25% of Bobl implied volatility.