Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Today, a German news magazine is moaning about the potential end of multilateralism and the risk of a currency war. However, one cannot agree with the view (which others have brought forward, too) that monetary policy as pursued by the major central banks (in particular the ECB) has always been tantamount to “exchange-rate manipulation”.

Monetary policy obviously has an impact on the exchange rate, and the exchange rate has an impact on monetary policy via imported inflation.

However, this has nothing to do with exchange-rate manipulation. That term, as used by economists, central bankers and (so far) policymakers, means something completely different. As a rule, monetary policy measures lead to a market-based, equilibrium exchange rate. If a central bank or a government tries to influence this equilibrium exchange rate, which is the result of its monetary policy and the monetary policies of all other central banks, it engages in exchange-rate manipulation.

While EUR has been resilient to the latest under-delivery from the region’s economy. But with the ECB no longer content to sit this out, the downside threat to EUR is becoming a more tangible. QE1 depressed EURUSD by 12% on the ECB’s own estimates.

Most obviously, the ECB is no longer as relaxed about the economy and lack of progress on inflation as it was. This could help to restore the missing link between economic performance and the currency, to the detriment of EUR.

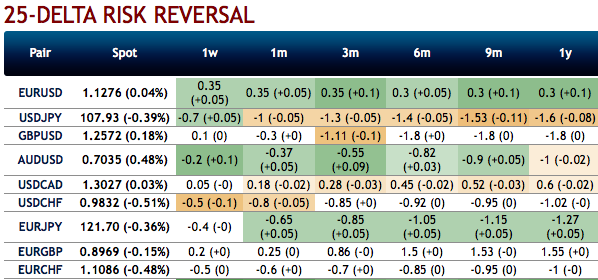

OTC Updates: Well, ahead of these events, let’s just quickly glance at OTC outlook before looking at the options strategies.

Bullish neutral risk reversals of EURGBP have been observed to the broader bullish risk outlook in the FX OTC markets, this is interpreted as the hedgers are still keen on bullish risks but with mild downside risk sentiment in the near-term, while the pair displays 6.49-6.82% of IVs.

While positively skewed IVs of 3m EURGBP options have been balanced on either side, bids for both OTM calls and OTM puts. This is conducive for options holders of both OTM call and put options.

While EURGBP risk reversals of the existing bullish setup remain intact, even if you see any abrupt negative risk reversal numbers, it should not be perceived as the bearish scenario changer. Instead, below options strategy could be deployed amid such topsy-turvy outlook.

3-way options straddle versus ITM calls seem to be the most suitable strategy for EURGBP contemplating some OTC sentiments and geopolitical aspects.

Options Strategy: The strategy comprises of at the money +0.51 delta call and at the money -0.49 delta put options of 2m tenors, simultaneously, short (1%) ITM puts of 1w tenors. The strategy could be executed at net debit but with a reduced trading cost.

Hence, on hedging as well as trading grounds, initiate above positions with a view of arresting potential FX risks on either side but slightly favoring short-term bearish risks. Courtesy: Sentrix, Saxo and Commerzbank