Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

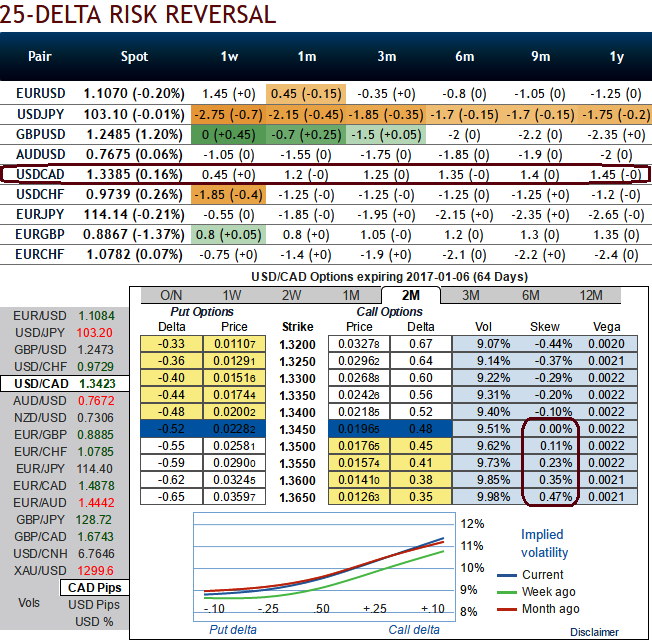

The fact that market attention will focus less on the US labour market report today may mean that the Canadian labour market report receives more attention.

We doubt whether this will turn out to be quite so positive for CAD.

The currency is suffering as a result of the falling oil price anyway and following rising employment in August and September there is likely to be a notable countermove in October which would be expected to put pressure on CAD.

OTC outlook:

We reckon the above fundamentals seem to be reasonably addressed by hedging participants, as you can observe the risk reversal flashes for 1 and 3 months tenors, although we see neutral changes to the bullish risk sentiments, as a result, USD seems to be gaining in next 2 months tenor on recent OPEC’s announcements, on account of series of significant data events such as the US presidential polls and on the eve of Christmas where Fed’s chances of hiking can’t be disregarded.

Mounting positive skews in 2m implied volatilities suggests RKO calls on speculative grounds, the USDCAD 2-3m skew has been bid with Trump progresses in the polls, lifting it to its highest level since June 2015.

Speculative call:

Given the vol surface set-up, we see two possible option constructs to play the resulting grind higher in USDCAD but taking minor bear swings in consideration:

i) USD call/CAD put vol flies are severely depressed, much more so than ATMs (see above chart); 1*2*1 USD call/CAD put flies are therefore natural expressions of slow and steady CAD weakness.

For instance, a 3M 1.33 /1.36 with 1.39 RKI/1.39 USD call/CAD put 1*2*1 butterfly (at spot ref: 1.3342), and delivers 4 times maximum payout ratio if the RKI triggers, 9.5 times if it does not.

ii) As an alternative, one could also short shorter-dated strangles to finance the purchase of longer-dated USD call spreads and exploit the inversion of the term structure.

For instance, one could mull over shorting 1M 1.29/1.35 strangles to finance the purchase of 3M 1.33/1.36 call spreads, a nearly 75% cost savings to buying the standalone call spread.

Hedging Framework:

Strategy: 2m 3-Way Diagonal Straddle versus OTM Put

Spread ratio: (Long 1: Long 1: Short 1)

Rationale: Let’s glance on sensitivity tool for 2m IV skews would signify the interests of OTM call strikes that means the ATM calls higher likelihood of expiring in-the-money, so writing overpriced OTM puts would be a smart move to reduce hedging cost.

The execution:

Go long in USDCAD 1M at the money -0.49 delta put, and go long 2M at the money +0.51 delta call and simultaneously, Short 2W (1%) out of the money put.