Philippine GDP Growth Slows to 2.3% in Q2

Philippine GDP Growth Slows to 2.3% in Q2  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan

Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan  Oil Prices Surge as Iran Hormuz Restrictions Renew Supply Fears

Oil Prices Surge as Iran Hormuz Restrictions Renew Supply Fears

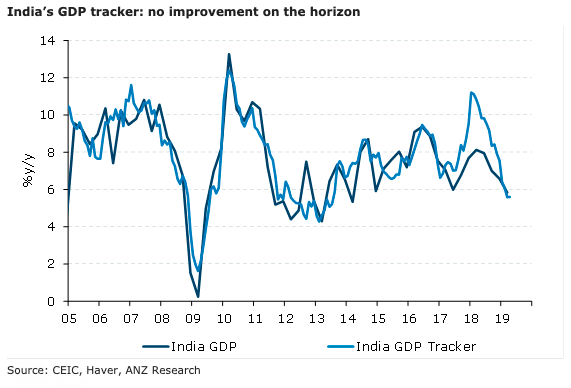

In line with the weakness in Q4 FY19 (quarter ending March 2019) GDP print, India’s FY20 GDP growth is expected to be even slower at 6.5 percent y/y, according to the latest report from ANZ Research.

The general activity and consumption indicators show no let-up. Investment indicators provide some green shoots (like credit to industry and investment proposals), a sustained recovery is however, missing.

The growth slowdown, amid weakness in demand pull inflationary pressures is likely to see the Reserve Bank of India (RBI) cut rates further this year, with expectations of a further 75bps of cuts in the next six months.

However, the bigger risks to this view come from a continued slowdown in manufacturing and consumption indicators and trade-related uncertainties which could impact the export outlook.

While the adverse effects of India’s relegation from the GSP (Generalised System of Preferences) programme will likely be limited given its low coverage, an escalation (India has retaliated with higher custom duties on 28 US products) could be unsettling, the report added.