Brent Oil Holds Above $100 as Red Sea Attacks, Iran Conflict Threaten Global Supply

Brent Oil Holds Above $100 as Red Sea Attacks, Iran Conflict Threaten Global Supply  European Regulators Clash With U.S. Treasury Over Private Credit Transparency

European Regulators Clash With U.S. Treasury Over Private Credit Transparency  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Japan’s Nikkei Slides Over 2% as Alphabet Selloff Sparks AI Spending Concerns

Japan’s Nikkei Slides Over 2% as Alphabet Selloff Sparks AI Spending Concerns  India to Continue U.S. Trade Talks After Trump Imposes 10% Import Tariff

India to Continue U.S. Trade Talks After Trump Imposes 10% Import Tariff  BOJ May Raise Japan Growth Forecast While Keeping Focus on Inflation Risks

BOJ May Raise Japan Growth Forecast While Keeping Focus on Inflation Risks  ECB's Kocher Says No Inflation Spillover Yet From Iran Conflict, Warns Risks Remain

ECB's Kocher Says No Inflation Spillover Yet From Iran Conflict, Warns Risks Remain  Iran Rejects U.S.-Backed Ceasefire as Trump Escalates Military Threats, Oil Tops $100

Iran Rejects U.S.-Backed Ceasefire as Trump Escalates Military Threats, Oil Tops $100  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

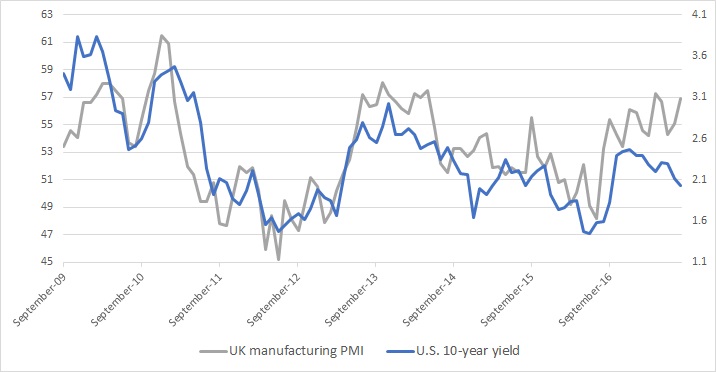

The above four charts show the relation between U.S. 10-year yields and manufacturing PMI numbers from the United States, Switzerland, Eurozone, and United Kingdom. We have chosen U.S treasury as a representative of global yield due to the importance of the U.S. dollar in the global financial system. Even if we had chosen 10-year yield from each region, the outcome wouldn’t be starkly different.

All four charts are showing the close relationship between the manufacturing PMI and 10-year yields, which is not surprising given the fact that central banks do not have much influence on the long term yields, unlike the short-term yields. Long-term yields like 10-years depend on the inflation outlook, state of the economy, savings glut etc.

All four charts have recently been flashing warning signs. A continuing divergence is quite visible for all four charts; extreme for Eurozone. It can be seen that while manufacturing PMI is moving higher, the 10-year treasury yields have been moving lower. For the United States, the divergence began last December and still continuing. For Eurozone, it began back in September 2015. For the UK, the divergence began in 2015, it closed somewhat last year but the gap started widening again since December. For Switzerland, the divergence began December last year and still growing.

While a divergence is n not an all new phenomenon, as can be seen in the chart of U.S. ISM manufacturing PMI and 10-year yields. Back in 2014, a divergence occurred. From March to October 2014, while PMI grew, U.S. treasury yield headed lower. But the divergence collapsed with a slowdown in the economy. So the real question is ‘what will happen this time around? Will yields move higher or will economy slow down?’