Gold Price Holds Weekly Gain as Middle East Tensions and Fed Rate Outlook Drive Market

Gold Price Holds Weekly Gain as Middle East Tensions and Fed Rate Outlook Drive Market  Japan Manufacturing Growth Holds Strong in July Despite Middle East Uncertainty

Japan Manufacturing Growth Holds Strong in July Despite Middle East Uncertainty  Iran Rejects U.S.-Backed Ceasefire as Trump Escalates Military Threats, Oil Tops $100

Iran Rejects U.S.-Backed Ceasefire as Trump Escalates Military Threats, Oil Tops $100  India to Continue U.S. Trade Talks After Trump Imposes 10% Import Tariff

India to Continue U.S. Trade Talks After Trump Imposes 10% Import Tariff  Trump Says No Decision on Major Iran Strikes as U.S.-Tehran Talks Intensify

Trump Says No Decision on Major Iran Strikes as U.S.-Tehran Talks Intensify  US-Mexico USMCA Talks Advance as Auto Rules Remain Major Sticking Point

US-Mexico USMCA Talks Advance as Auto Rules Remain Major Sticking Point  Asian Stocks Slide as Oil Tops $100, Middle East Conflict Fuels Inflation Fears

Asian Stocks Slide as Oil Tops $100, Middle East Conflict Fuels Inflation Fears  Australia Jobs Surge in June Strengthens Case for More RBA Rate Hikes

Australia Jobs Surge in June Strengthens Case for More RBA Rate Hikes

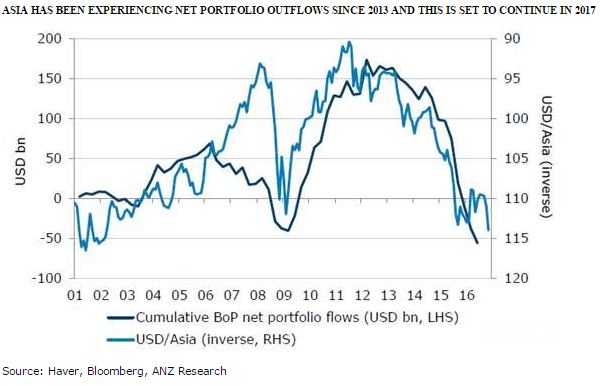

Asian currencies are expected to depreciate for the fifth straight year, going into 2017, following mounting global headwinds; also sharp appreciation in the greenback will pose serious threats to major Asian currencies.

Rising US interest rates on the back of continued policy normalization by the US Federal Reserve and prospects of fiscal stimulus from a Trump administration is set to keep the USD bid. Asian economic growth should eventually benefit from a better performing US economy. But a stronger USD and rising US yield environment tends to cause volatility in capital flows and pose a headwind to Asian currencies.

Further, there remain potential risks from a rise in the Chinese yuan, although Chinese authorities have put up efforts to keep the RMB index stable. According to the report, ANZ remains bearish on both KRW as well as SGD. The real effective exchange rates of both currencies are elevated given the state of their economic cycles. A re-centring of the policy band by MAS is likely in 2017.

INR’s and IDR’s macroeconomic fundamentals have improved such that they are less vulnerable to rising US yields compared to the taper tantrum period. But with both countries running higher inflation rates compared to their trading partners, some nominal currency weakness can be expected, though this is compensated by their higher yield.