U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

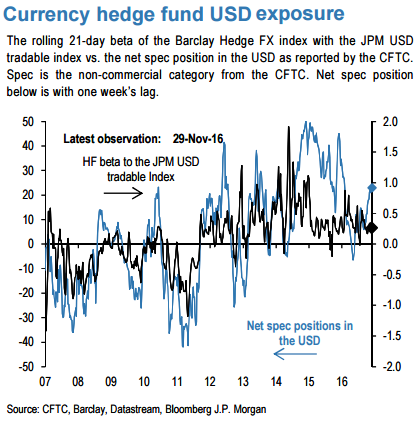

The above performance picture, we get from the monthly reporting hedge funds is quite disappointing than the picture from the daily reporting funds as even currency hedge funds performed poorly in November.

As you could observe the rolling 21-day beta of the Barclay Hedge FX index with the JPM USD tradable index vs. the net spec position in the USD as reported by the CFTC. Spec is the non-commercial category from the CFTC. Net spec position below is with one week’s lag.

Fed package: The FOMC proved more hawkish than markets anticipated, with the dots shifting to reflect a total of three hikes during 2017. This hawkishness helped to mitigate some of the underperformance of treasury yields such as ZAR 10-year payer trades, as rates were paid up across emerging markets while EM currencies deteriorated.

Over the near term, some positive political dynamics and technical forces may continue to bolster ZAR resilience. Domestic and external factors point in divergent directions, underscoring the importance of trade entry levels.

ECB’s shift: An ECB tapering scenario by 2018, our house view, creates a big demand cliff for global bond markets in 2018, unless supply collapses at the same pace as demand, which seems rather unlikely, or demand outside G4 central banks picks up quickly, something that is more likely to happen only after a big increase in bond yields. An alternative scenario where the ECB tries to preserve ammunition would prolong QE to beyond 2018.

A smoother QE reduction profile is also important because this week’s ECB decision involved not only a reduction in the pace of purchases but also a shift in purchases towards shorter maturities which implies less duration withdrawal.

The USD surged higher, aligned with US yields on the back of the Fed not only raising rates by the expected 25bps, but increasing their expectations for three more hikes next year, from two. They expect jobs growth to strengthen further and inflation to pick up towards their 2% target.

As a result, Long-term the move down through the 1.0450 region is arguably the last in the cycle from the 1.6020 highs set back in 2008. If this is the case the market should not breakdown through the 1.01-0.99 region. Such a move would expose a deeper rift in the EUR and risk a move towards 0.90.