European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

Amid the overhang from global trade tensions, the dollar fell against the EUR, GBP, and CHF as rhetoric out of China (from the Commerce Ministry on Friday) grew increasingly strident. Note however that the cyclical closed largely flat against the USD and trailed their G10 peers.

This week, FOMC minutes are due on Wednesday while Fed appearances are penciled in from Tuesday to Friday. On this front, watch for further Fed rhetoric with respect to the potential deleterious effects of a global trade war, with the attendant tempering of rate hike projections.

The currency markets navigated two major events over the past week that left the broad dollar with no more directional clarity than before. The March FOMC under new Fed Chair Powell raised rates as widely anticipated and forecast an additional one-and-a-half rate hikes by the end of 2020, but any hawkish fallout for the dollar was contained by and the back-loaded nature of projected rate increases and only a marginal upward revision to the implied neutral real rate relative to the December’17 SEP.

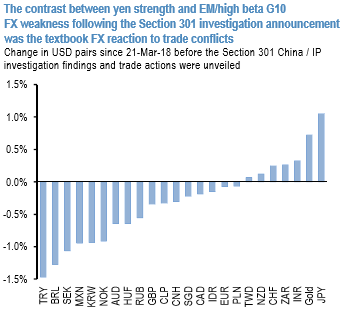

Any designs of re-loading USD-funded carry trades on this relatively benign FOMC outcome, especially given the recent spate of soft-side US inflation prints that had allayed fears of a behind-the-curve Fed, were however frustrated by the announcement of US trade actions following the findings of the Section 301 China/IP investigation that hit equities harder than anticipated.

The 3%+ tumble in SPX after the release led to predictably sharp rallies in JPY and gold and declines in EM and high-beta G10 (refer 1st chart), and validated our trade protectionism template of decoupling between reserve and non-reserve FX that we have frequently cited in these pages.

The trades portfolio has run relatively light on risk in recent weeks, with a slight defensive lean predicated on navigating the uncertainty of potentially disruptive US trade policy. This has helped sidestep head fakes in risk markets such as that following benign US CPI, but has also missed participating in the extension of the yen rally after taking profits on AUDJPY shorts (in hindsight) too early around the VIX shock.

Having been sidelined in the yen since then in anticipation of a seasonal uptick in unhedged Japanese outflows in the new fiscal year, we are cautious about chasing USDJPY lower from current levels, especially without the tailwind of broader dollar weakness.

Long reserve FX exposure is instead focused in two of the relative laggards – EUR and CHF – via longs in EUR/antipodean crosses and a short in USDCHF that eked out only workmanlike gains over the past week but offer potentially more durable returns on divergent monetary policy cycles even if trade tensions ebb. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: